AI Costs Surge 10x Despite Token Price Drops as Companies Grapple With Usage Explosion

10 Sources

[1]

AI is becoming a bargain hunter's market, with a few luxury models on top

The price of AI tokens is fluctuating widely, with some becoming cheaper and others more expensive, leaving users of AI services struggling to assess if the price is right. Aman Panjwani, an AI engineer based in India, says that GPT-4-class model output cost about $20 per million tokens in late 2022. Today, equivalent capability costs about $0.40, a 55x decline in less than four years, he said, citing Introl's December 2025 unit-economics analysis. "When DeepSeek released its R1 reasoning model in January 2025 at $0.55 per million input tokens and $2.19 output - against OpenAI's o1-preview at $15 and $60, launched just four months earlier - the entire market repriced overnight," Panjwani said in an analysis provided to The Register. "A 97 percent discount tends to do that." During this same period, prices for cutting-edge frontier models surged. "OpenAI doubled the price of GPT-5.5 to $5 input and $30 output per million tokens - that's on its own pricing page," said Panwani. "Google's Gemini Flash 3.5 arrived three to six times more expensive than the model it replaced." The recent release of Anthropic Claude Sonnet 5 continues that trend. Even though its per-token price is lower than Claude Opus 4.8, it uses more tokens to produce the same results. Anthropic's Mythos and Fable models are also quite costly, when available. Also this year, Anthropic moved corporate customers away from per-seat pricing to metered pricing and limited permitted uses of its subsidized subscription plans. Panjwani argues such moves show the token market is splitting in two, with commodity inference heading toward zero even as frontier inference costs rise. Ameya Kanitkar, CTO of Larridin, an AI measurement platform, said that about six months ago, AI costs were a primary concern because companies spent between $20 and $100 per month per LLM subscription. But around February, AI services vendors companies began pushing for more AI usage at a time when the models were getting better and could handle more complex agentic work that takes longer to complete. "On average we have seen the cost go up about 10x between January and now, especially in engineering ops," Kanitkar said in an interview with The Register. It's a change he attributes to the shift toward longer, agentic tasks and metered pricing. "The new trend that is emerging is that the open source models, open weight models are actually not that far behind the frontier models," he said. "And now the costs are hitting the balance sheet, which are not the real costs, companies have started truly thinking, 'okay, how can we actually adjust these costs?'" Kanitkar said he's seeing companies spending between 10 and 20 percent of their labor cost - e.g. $2,000 to $4,000 per month for a software engineer paid $200,000 annually - on tokens. But, he added, higher spending doesn't necessarily mean higher productivity. Between 15 and 30 percent of AI users among Larridin's clients account for more than 50 percent of total AI spend, and often that spending does not correlate with gains in output, according to a company spokesperson. When Larridin plotted token spend against developer productivity, it found an inflection point at about 35 to 40 percent of client spending where burning more tokens failed to boost productivity. Using that point as a token limit for employees can cut AI costs by 40 percent without changing anything else, Kanitkar said. Open weight models offer another cost lever. Kimi 2.6/2.7 and GLM 5.2, Kanitkar said, "are almost at parity with Opus4.7 or 4.8. And they are 10x cheaper in theory, or about 5x cheaper in practice. They tend to be a little bit slow and they tend to consume more tokens on the pure token basis - that costs more, but the token cost is low." Kanitkar said he's now seeing almost 75 percent of companies use multiple models. Switching back and forth, he said, is more difficult for customer-facing agentic work, but for software development, it's much more viable. Even so, price isn't always the most important consideration. Larridin data shows that enterprises still direct almost half of their AI spending toward Anthropic's Opus model because it handles complex engineering and reasoning tasks well. ®

[2]

Employers pushed staff to use AI more. That has backfired

Some Amazon developers must be suffering whiplash about how they use AI. The technology group sets targets for most of its developers to use AI tools. This year it started monitoring consumption and posting usage figures on internal leader boards. But after the FT wrote in May that some workers were automating non-essential tasks to improve their ranking, Amazon took the leader boards offline. "Please don't use AI just for the sake of using AI," Amazon senior vice-president Dave Treadwell told staff. The shift was a sign of how employers are already changing how AI should be used and incentivised. As model providers switch from subscriptions to token-based billing, the cost of profligate usage is starting to hit home. Using leader boards and embedding token use in performance reviews is "a really stupid way to do anything", Jacob Lauritzen, chief technology officer of legal AI firm Legora, told the 20VC podcast last month. "Reward [staff] for being effective and efficient and having more output, not for necessarily using AI." After the public launch of OpenAI's ChatGPT in 2022, many corporate workers worried first about being caught "cheating" by using the powerful new tools. They were more likely to conceal their usage than boast about it. As the possibilities of generative AI became apparent, though, companies started to encourage wider use. In April 2025, for instance, Tobias Lütke, chief executive of Canadian ecommerce platform Shopify, set "reflexive AI usage" as "a baseline expectation", building it into performance reviews. It said teams asking for additional staff would have to demonstrate why AI could not fulfil the task. Microsoft made AI use among developers mandatory and set usage as a core measure in employee appraisals. Consultancy Accenture said last year that workers who could not upgrade their skills for the AI age would be "exited". By this February, it was tying the promotion prospects of senior staff to usage of its AI tools. Shoosmiths, the London-based law firm, offered a firm-wide £1mn bonus if staff logged 1mn prompts on Microsoft Copilot in the year to March. This era of experimentation has given way to "tokenmaxxing", with staff competing to use as many tokens as possible. The drive to delegate more tasks to AI, and to link the use of the new tools to employee reviews, has already disconcerted workers, and not only because they fear it threatens their own jobs. "They are pushing us to adapt our problems to the tool rather than the other way around. We're in a 'move quickly, adopt it fast, we'll see where we are later' mode," says one systems engineer, who prefers to remain anonymous. He adds that those embracing the approach can win recognition, but that the campaign has led to AI-induced errors that are time-consuming to repair. Another senior back-end software engineer says he is "quite unhappy" about AI usage as an official performance measure: "It removes my choice . . . It should be up to people like me to decide what's the best tool to use. I don't feel I should be penalised for not using a tool I don't feel like using." Ravin Jesuthasan, senior partner and global leader for transformation services at the human resources consultancy Mercer, says: "This year for the first time I started to see a maturing of the AI conversation. Now we need to see a return on it, rather than spraying and praying." Speaking at an FT webinar on AI adoption last week, Tanuj Kapilashrami, chief operating officer at bank Standard Chartered (and co-author with Jesuthasan of the 2024 book The Skills-Powered Organization), said: "I think the days of 'let a thousand flowers bloom', tech for the sake of tech, encouraging experimentation without it being rooted in the real commercial realities of your business . . . are gone for most businesses." Still, capping technology use is anathema at some companies whose prospects are firmly tied to the surge in AI use. Nvidia's chief executive Jensen Huang told the All-In podcast in March that he worried about his engineers using too few AI tokens. If an engineer being paid $500,000 a year "did not consume at least $250,000 worth of tokens, I am going to be deeply alarmed", he warned. Jon Lester, IBM's vice-president of HR technology, data and AI, says: "For us, limiting innovation by putting arbitrary targets and limits on certain things is a very difficult conversation to have. We want [our] 270,000 people to come up with ideas they haven't had and deliver the next innovation that will change the way we work." As the costs of token usage increase and companies start to impose caps on AI use, some companies are putting in place routers that direct basic queries to open-source large language models or to less token-intensive AI versions. They are also developing more sophisticated ways to encourage the right sort of AI use. Boston Consulting Group's Kristy Ellmer, co-author of How Change Really Works, says that instead of putting "a dollar value on creating a new ChatGPT skill, [you should ask] 'how many people are actually using that skill? Is it really creating value?'" Rob Fisher, vice chair of professional services firm KPMG in the US, says: "I've always been a believer that carrots are quite a bit more powerful than sticks and so I think we've tried to try to lean more to carrots." KPMG offers a dashboard where staff can compare usage and has instigated a quarterly "AI Spark" award for the brightest AI innovations. AllianceBernstein has installed a different set of incentives to encourage its asset managers to challenge the output of chatbots. "We say, how many times did you challenge what AI said? How many times did you override what it said? Did you capture that decision? Were you right most of the time? Were you wrong most of the time?" Andrew Chin, chief artificial intelligence officer, told the FT's webinar. IBM ties its incentives to its training and development programme. Ten years ago, the group set a target of at least 40 hours of training a year for each employee. At that point the number of hours of actual training being done was 31 per worker. That has since increased to 87 and the target has been removed. The expectation is that "you will use [AI tools] to improve your productivity as an employee or as a team", says Lester. Usage and outcomes are monitored but there is no formal incentive -- although Lester says the company may go back to staff and say "our estimate would be that this [tool] should save you time; could you tell us as a group or a team why you aren't using it?" Shoosmiths' 1,200 staff hit their 1mn prompts target with four months still to run and claimed their bonus (the firm's 200 partners joined the AI push but were paid through a separate rewards scheme). The firm asked workers not to use AI to create images, partly to mitigate the environmental impact, and only to employ Microsoft's Copilot for "the business of law" -- such as research and drafting emails -- not "the practice of law". Otherwise, they were free to experiment. "We just wanted people to use the technology; we were less concerned about what they did with it," says chief executive David Jackson. "We always knew that in year two it was going to be about AI fluency." The next firm-wide bonus will be paid if staff hit a target for accreditations to a tiered training scheme. Jackson says the firm has not asked people to slow down their prompting as token costs increase, "but because we're talking about purposeful usage, that's taken care of itself".

[3]

Token maxxing is your AI program's quiet failure mode

Most organizations have settled on those numbers because they're easy to track and show up well in reports AI investment is accelerating across enterprises. Budgets are increasing, boardrooms are asking hard questions, and the answer they're getting back is token costs, prompt counts, and copilot deployment numbers. Those aren't business metrics. They're activity logs. Most organizations have settled on those numbers because they're easy to track and show up well in reports. The problem is that those numbers measure the activity, not the results. They show how much AI is being used, not whether the business is doing better since implementing it. This is where token maxxing starts. It happens when organizations begin rewarding those who use AI the most, rather than what it actually delivers. By optimizing for the wrong thing, we're quietly setting AI programs up to fail. When metrics become the mission There's a simple truth in business: people optimize for what gets measured, and we're seeing that with AI right now. Understandably, because teams begin to generate more output when that is what leadership tends to see and reward. Over time, the measure becomes the mission, and the focus on real outcomes starts to drift. The result is a surge in output that looks impressive on paper but has little to do with faster decisions or better products. Teams with the highest usage or spend start to become the benchmark that others feel they need to match. But metrics like token spend should be evaluated the same way any other business investment is. If we committed the same budget to a new sales tool or a go-to-market campaign, the first question from the board would be: how did revenue increase, and did it move the business forward in a measurable way? High token consumption with no clear line to a business outcome is not a success story. Without that connection, it is just an additional cost. Meanwhile, the organizations that figure this out first will move faster with less spend -- and that gap compounds. AI did not create the problem; it exposed it We've seen this pattern before. In the early days of cloud computing, companies moved fast and invested heavily without rethinking how work was structured. Costs went up, but the outcomes didn't always follow. That wasn't a cloud problem. And this isn't an AI problem. It never was. The reality is that most companies already had a structural issue long before AI arrived. The work that matters most doesn't live in a single system. It stretches across teams, tools and departments, held together by people stitching context together and filling in the gaps between systems. That's always been the case. What AI has done is expose it, and this is where the problem runs deeper than just metrics. AI makes individuals faster within the tools they already use. But when that work still sits inside disconnected systems, speed doesn't fix the problem; it makes the gaps more visible. Teams move faster, but not necessarily together, and that's why usage metrics can look so strong. More prompts, more output, more activity. On the surface, it looks like progress, but without a clear connection to outcomes, that activity can quickly become noise. The problem isn't just that we're measuring the wrong thing. It's also that most organizations don't have a clear view of outcomes in the first place. What good measurement looks like Stop asking how much AI is being used and start asking what has changed because of it. A few shifts that will follow: Output volume does not equal business value. Treat the two as interchangeable, and your AI program is already starting to drift. Start with the outcome, not the tool. Instead of asking, "How many prompts did we run?" ask, "What did we achieve?" Measure what crosses teams. If impact stays inside a single function, you have a useful tool -- not a competitive advantage. Here are a couple of examples: for engineering teams, this could mean focusing less on lines of code or pull requests and more on what actually reaches production and delivers value to customers. For marketing, it might be focusing on whether campaigns launch faster or land better. Ultimately, AI that makes one person's morning easier is a useful tool, but real value comes from AI that changes how the whole company gets work done. Without that, you end up with intelligent tools that operate in isolation. Helpful in moments but limited in impact. Redefine what good looks like Right now, most of the AI conversation is still focused on individual productivity -- how much faster one person can write, code, analyze, or create. That matters. But it's only part of the story. The bigger opportunity sits at the organizational level and looks at how work actually moves across teams, systems and the company as a whole. AI can absolutely improve how businesses operate, but only if we are willing to ask harder questions about what we are actually measuring and why. The companies that pull ahead won't be the ones using AI the most. They'll be the ones who changed what they measure when AI showed up. That's the only metric that matters. Use the best business cloud storage to manage your data. This article was produced as part of TechRadar Pro Perspectives, our channel to feature the best and brightest minds in the technology industry today. The views expressed here are those of the author and are not necessarily those of TechRadarPro or Future plc. If you are interested in contributing find out more here: https://www.techradar.com/pro/perspectives-how-to-submit

[4]

DeepSeek cut prices 75%. The 100x problem remains

DeepSeek's recent decision to drastically cut pricing on its V4-Pro model by 75% should have been unequivocally good news for enterprise AI vendors and developers. Instead, many are discovering that cheaper models don't automatically translate into healthier margins. The reason is simple: While inference costs plummet, agent systems are voraciously consuming tokens faster than prices are declining. For the last 2 decades, software economics was dictated by the same rule. Infra became cheaper every year whereas applications became more capable. AI was initially hypothesized to follow the same pattern. As frontier models improved and token prices dropped, many assumed inference would become a negligible operating expense.That assumption has begun crumbling exponentially. A chatbot usually turns one user question into one model call. An agent turns it into a chain of planning, retrieval, tool use, verification, summarization, and follow-up decisions. The user sees one answer. The vendor pays for the loop. That is the 100x problem: The same user-visible request can cost a lot more to serve as an agentic workflow than as a chatbot or retrieval-augmented generation (RAG) response. In longer-running workflows, the multiplier is higher. Falling model prices help, but they do not fix a product architecture that turns one prompt into dozens of billable operations. The scale of what is now at stake is clear in how model providers themselves are pricing developer relationships. OpenAI's proposed program to give every Y Combinator startup $2 million in API credits -- a number that would have funded an entire seed round in any prior tech cycle, and when the same cohort got by on a few thousand dollars of AWS credits -- is less a recruiting perk than an admission of what it now costs to run an AI-native company through its first year of product. For established enterprises retrofitting agents into existing product lines, the absolute numbers are larger still. What token amplification is In a single-turn chatbot, one user message produces roughly one model call. Input-to-billed ratio is about 1:5. In a multi-step agent rolled out across customer support, sales operations, finance, legal review, and engineering, that ratio routinely lands at 1:700 or higher. Every loop iteration carries forward the cumulative conversation, tool outputs, and reasoning traces. Each step appends; nothing is dropped. A "simple" agent query like "What did our top customer ask about last week?" typically touches seven priced operations before returning an answer: One sentence in, roughly 35,000 input tokens billed. Somewhere between $0.10 and $0.40 per query on a frontier model. Multiply that by a million queries a month -- the table-stakes volume for any enterprise B2B feature -- and the line item is six figures. Why this breaks the existing AI business model The dominant pricing story for enterprise AI has been seat-based SaaS: Pay per-user per-month, deliver agent capability, capture margin. That model assumes a reasonably bounded cost-per-user. Token amplification breaks the assumption. A power user running 50 agent invocations a day on a $40/seat plan can cost more in inference than the plan charges. Token amplification shatters the traditional SaaS pricing model. When a power user's daily agent activity costs more in inference than their monthly subscription fee, vendor gross margins turn negative, a paradox that compounds as customers deepen their agent adoption, the very usage curve vendors are selling to their boards. Several vendors are now privately reporting negative gross margins on heavy users, mirroring recent cloud expenditure reports from the Bessemer 'Supernova' cohort, where the correlation between AI-agent adoption and gross margin contraction has moved from a theoretical risk to a primary P&L headwind. The visible symptoms have started leaking into public coverage. Bloomberg this week documented a widening gap between Salesforce's Agentforce marketing demos and the capabilities actually shipping to customers. This is the kind of gap that opens predictably when promised functionality is technically possible but uneconomical to serve at the price the seat plan implies. Salesforce is the most-watched case, not a unique one. "For my team, the cost of compute is far beyond the costs of the employees." -- Bryan Catanzaro, VP of Applied Deep Learning, Nvidia The strategic implication is not "AI is expensive." It is that the dominant business model assumed by most AI-native company plans does not survive contact with agentic workloads. A simple example Consider an enterprise software vendor charging $40 per-user per-month for an AI-enabled support assistant. A traditional chatbot might cost only a few cents per user per day in inference, leaving healthy gross margins. Now replace that chatbot with a fully agentic workflow capable of investigating tickets, querying internal systems, drafting responses, validating outputs, and escalating exceptions. If a heavy user executes 50 to 100 agent requests per day, inference consumption can increase by an order of magnitude. What was once a negligible infrastructure cost becomes a material operating expense. This creates an unusual dynamic: The customers receiving the most value from the product are often the customers generating the highest inference costs. In extreme cases, vendors can find themselves with their most engaged users contributing the least profit. The result is a growing realization across enterprise software that agent adoption and margin expansion are no longer automatically aligned. Agent orchestration is the new moat The technical responses are known and converging. They are not novel, but they are critical for survival * Cost-aware routing: This technique involves a small classifier model that decides which tier (Haiku, Sonnet, Opus equivalents) handles each query. Well-tuned routers cut inference bills by around 60% without any degradation in quality * Prompt caching: Anthropic, OpenAI, and Google now offer 75 to 90% discounts on cached prefixes. * Context discipline: You can truncate tool outputs, prune reasoning traces, and cap tool depth to prevent your agent from going down a rabbit hole * Speculative decoding: for self-hosted deployments, this technique guarantees 2 to 3X effective throughput on the same GPUs. "Organizations using orchestration-led governance report stronger productivity gains -- a holistic orchestration layer is associated with six times greater productivity impact than compliance‑only approaches" -- IBM The companies building this layer well are starting to look less like microservice operators and more like financial trading systems: Every routing decision priced, every path with its own P&L, every tenant on a metered budget. What enterprise leaders should actually do Four moves separate the companies that will still have margin in 24 months from the ones that won't: The next 24 months The structural shift underneath agentic AI is not that it is expensive. As DeepSeek's price cut today underscores, frontier inference unit costs are dropping roughly 3X per year, and the curve is not slowing. The shift is that amplification is outrunning the price cuts. Cutting per-token costs 75% does not help a company whose agents are doing 700X more tokens per user query than its pricing model assumed. For the first time since the cloud era began, architecture decisions are again financial decisions in real time. A prompt redesign is a margin event. A poorly bound agent loop is an outage with a credit card attached. The companies that survive the next 24 months of AI infrastructure pricing will not be the ones running the cheapest model. They will be the ones whose agents are smart and know what they cost to think. That is the 100X problem. And it is arriving faster than the price cuts can hide it. Maitreyi Chatterjee is a senior software engineer at a big tech company. Devansh Agarwal works as an ML engineer at a leading tech company. Welcome to the VentureBeat community! Our guest posting program is where technical experts share insights and provide neutral, non-vested deep dives on AI, data infrastructure, cybersecurity and other cutting-edge technologies shaping the future of enterprise. Read more from our guest post program -- and check out our guidelines if you're interested in contributing an article of your own!

[5]

Cognition CEO says tech companies got 'carried away' with token leaderboards and should measure employees on output instead | Fortune

The trend of tokenmaxxing has gone too far. That's at least according to Cognition CEO Scott Wu, who argues that as companies scramble to rein in AI spending, they should focus on employee productivity instead of AI use. In an episode of the "Founders" podcast with David Senra, Wu said that as companies are shelling out on token budgets, there needs to be a push to identify how AI is creating real value, which comes from defining clear returns on investment for the technology, including revenue growth, efficiency gains, or cost-saving. "It is directionally correct, but I think there are definitely some places where people have gotten carried away," Wu said of tokenmaxxing. "People are like, 'We rank our engineers by how many tokens they're spending.' Well, let's try and rank people by how much output they're actually producing." Cognition measures its success in how much it is able to increase engineering capacity. The AI software company is the creator of Devin, widely considered the first AI coding agent. Financial institutions like Goldman Sachs use the tool as an AI software engineer, while auto companies like Mercedes-Benz and Rivian use Devin for research and development. Wu's remarks come after reports of companies like Meta and Amazon creating internal incentives, such as employee leaderboards, to measure token usage to encourage workers to discover AI use cases. But rather than drive innovation, the use of tokens became excessive, with employees using AI just to boost their leaderboard rankings. The tech companies soon scrapped the internal tracking after employees deployed the bots to complete useless tasks, the Financial Times reported. "Please don't use AI just for the sake of using AI," Dave Treadwell, an Amazon senior vice-president, reportedly told staff. The tokenmaxxing trend has also taken a financial toll on tech companies, such as Uber, which burned through its entire AI budget for 2026 in just four months, and last month capped token spending for employees to $1,500 per month. Despite tokens becoming cheaper as the technology improves -- dropping 90% in price since 2023 -- companies' AI spending has actually increased, as a result of companies feeling emboldened to gobble up more tokens as they decrease in price. As AI spending balloons, Wu warns that those dollars spent are only as valuable as the benefits they create. "The GPUs are expensive, but if your engineers are actually able to ship three times more, then it's very clearly worth it," Wu said. "You just want to make sure you're doing it the right way." Why tokenmaxxing failed This lopsided spending-to-output ratio is what Boston Consulting Group (BCG) noted as a hallmark reason why AI wasn't creating productivity gains in the workplace. Employees don't know what to do with the time new tools have saved them. BCG's 2026 Global AI at Work report, which surveyed nearly 12,000 frontline employees, found that 42% of workers reported regular AI use saving them eight hours per work -- about one workday per week -- but 66% said they received little to no guidance on how to invest the time they saved, and half of respondents said they weren't spending that saved time on other strategic projects. David Martin, global leader of BCG's People & Organization practice, told Fortune that the workplace productivity paradox emerging alongside AI is actually a human-created problem of leadership not communicating clear goals around the technology. "Senior leaders are really struggling to articulate what the vision and strategy is on AI," Martin said. "Consequently, it increases employee fear. It makes it harder for them to even understand what objectives they're pushing for, and it trickles through to adoption, usage, and the like." Mirroring Wu's philosophy around identifying AI's ROI in specific workplace environments, Martin suggested C-suites and managers treat AI as any other novel workplace tool, weighing its potential benefits instead of treating it like a productivity panacea. "A lot of companies just gave AI to everyone, regardless of position, and I think now they'll say, 'Well, let's be more thoughtful about who has access, and what is the business case? And are we delivering on it, ultimately?'" Martin said. "Then holding people accountable to meeting their targets, just like they would anything non-AI that they've been doing for the past 100 years."

[6]

How to embrace the spirit of 'Tokenmaxxing' without breaking the bank

"Tokenmaxxing" - the idea that AI coding success comes down to using as many tokens as possible - is an appealing metric. Tokens are the fundamental unit that AI coding tools use to read, write, and reason. So on the surface, more tokens should mean more output, more productivity, and more impact. But when we analyzed 12,000 developers across 200 companies, the data revealed that while more tokens do correlate with more output, they come at a significantly higher price per unit. Some organizations are pushing software engineers to use as many tokens as possible, using leaderboards to promote the biggest AI users. But that's not a sustainable strategy. CFOs are starting to push back on uncontrolled AI spending and asking coders to show receipts. Leaders may be willing to spend money to move fast, but they can't do it without proving their engineering teams are having an impact. The best approach to "toxenmaxxing" isn't to blindly push for AI adoption. Instead, the best path forward for companies is to push AI coding adoption more broadly, moving more engineers into the middle of the curve while avoiding both underuse and expensive overconsumption. Why 'tokenmaxxing' doesn't scale We found that the top 10% of Claude Code users consumed about 10 times as many AI tokens as the median developer but produced only about twice the output. In other words, increasing token consumption does increase output, but not proportionally. The research also shows a small but growing group of power users dominating total token consumption. At the 90th percentile, users are burning around 225M tokens per week, about 3x what they were using six months ago, and about 7x the median. Many engineering leaders are now looking at their highest adopters and trying to figure out how to get the rest of the organization to the same level. That approach is misguided. With the cost per merged PR increasing from $0.28 at the lowest adoption tier to $89.32 at the highest, scaling extreme token usage simply cannot drive value. Instead, engineering leaders should focus on smoothing the curve. Broad, moderate token consumption is far more cost effective than having a small group of power users at one end of the spectrum and everyone else lagging behind. When most of the organization is operating in the middle of the curve, AI becomes a durable advantage: enough to drive real productivity gains but not so much that engineering teams burn money chasing marginal output. Maximize impact, not token consumption The organizations that burn through the most tokens aren't necessarily getting the furthest with AI. When token consumption is high, most are spent on automating manual tasks with tools like Claude, Copilot or Cursor. Developers essentially have a better tool to do the same kind of work as they did before. To really drive impact with AI, engineering organizations need to move towards new, truly agentic modes of working. However, agentic systems require major investments in IT infrastructure, including context engineering, orchestration, and sandboxed environments. Until organizations address these issues, the productivity gains will remain blocked by an "agentic barrier" that no amount of tokens can overcome. How established enterprises can follow the AI-native lead Conversations around AI and software development focus on coding, but writing code is just one part of an engineer's role. Taking a product to market also involves roadmap work, deployment, go-to-market enablement, and more. If engineers are spending tons of tokens on writing code as fast as possible, everything else needs to catch up. Changing roadmap cadence and accelerating sales enablement requires major cultural shifts that many organizations aren't prepared for. As a result, extra cadences are often poured into the backlog or other things that may deliver value down the line but won't move the revenue needle in the short term. Teams can consume millions of tokens every week but have little to show for it by the end of the quarter. AI-native companies are more likely to see an immediate return on their AI investments. While established enterprises may not be able to start from scratch, adopting AI-native principles can help remove bottlenecks and turn token spend into measurable business returns faster. By designing workflows with automation in mind, they can continue to accelerate coding without creating technical debt. "Tokenmaxxing" is having a moment, but engineering leaders need to move beyond token count and start finding ways to prove value. By measuring how AI impacts delivery, quality, and productivity across the software delivery life cycle, leaders can demonstrate ROI and make sure every token counts. We've featured the best no-code platforms. This article was produced as part of TechRadar Pro Perspectives, our channel to feature the best and brightest minds in the technology industry today. The views expressed here are those of the author and are not necessarily those of TechRadarPro or Future plc. If you are interested in contributing find out more here: https://www.techradar.com/pro/perspectives-how-to-submit

[7]

Enterprise hits and misses - harness engineering takes over enterprise AI, and tokenomics is in full swing

Last week, I addressed reader pushback on my real-time organizational truth missive. I also unfurled something of a call to action: * Studies have shown that smaller models can reduce LLM operating costs by as much as 90 percent. * Even Google just admitted, in a major new playbook, that proper context/harness engineering accounts for 90 percent of the value of an agentic system, with the model accounting for just 10 percent. With AI tokenomics suddenly an overriding concern (read on for more), what better time to for enterprises to bear down on this? Now, we could get very semantical about where "context engineering" ends and "harness engineering" begins, and which is a subset of which, but does that type of wonkiness really matter right now? My recent work focused more on the AI context part; I issued a exhortation for a different, more ambitious, and more honest conversation about both the fragility of context AI agents rely on - but also the potential impact. But: surrounding that real-time context are all kinds of necessary agentic systems, from deterministic "verifiers" to authorization rules the agent should follow. The savvy construction of these systems has become a YouTube obsession amongst AI engineers. Ian's most recent piece fills in the gaps I left, and then some. So, Ian, what is an agentic harness? A typical harness is just a set of ordinary software components deployed around the model -- agent instructions written in plain-language documents, a filesystem for keeping track of what the agent needs to know over time, a command line for executing code or using tools, and a sandbox for keeping the agent away from things you don't want it to touch. And then, simplistically, a loop that repeatedly triggers another round of interaction between the harness and the LLM until the work is done. Well that sounds useful, but not really buzzword-worthy. But maybe that's the point? As Ian points out, one harness doesn't fit all. For enterprises, that's where the action is: An enterprise platform offers immediate access to the data, permissions, workflows and integrations already sitting inside that platform -- but may also pull the agent's operating logic deeper inside one vendor's architectural boundaries. Which is why many organizations may become increasingly interested in building their own harnesses using the growing range of developer frameworks and software development kits -- giving them more control over the purpose, decisions and governance of their agents, but also leaving them more deeply involved in engineering, securing and operating them. If you want agents that respect your permissions and adhere to your workflows, you're going to need to invest in your harness. Ian again: The harness is where purpose, operating rules, permissions, memory, economics and controls are actually encoded for a given type of agent. It determines what an agent knows, what it remembers, what it can access, what it is allowed to do and how it behaves when things go wrong. I'll take it further: harnesses may be a core/basic infrastructure, but mastering harness engineering is going to be a big deal - and a huge factor for companies that want less economic dependence on frontier model pricing. Granted, agentic loops, a.k.a. completing the next step in an agentic task or process, will not be found in the tech bargain bin anytime soon. But: a well-constructed harness will control that looping, and perhaps help route some of those "loops" to smaller/more affordable models - or terminate them if needed. I argue we've been giving LLMs too much credit of late, and not enough credit to well-designed harnesses - and the third party functions that enhance them. Claude Code, obviously one of the most successful productized LLM advancements of the last two years, is dependent on a well-designed harness to do what it does, as well as potentially deterministic components that harness makes available. Just how dependent is subject to debate and further research, but we have some ideas now, based on the Claude Code leak. It will take more research to settle the Claude Code neuro-symbolic debate - that doesn't matter here. So what does matter? How about building cool/useful, well-governed things without tokenmaxxing? The point is: models get much more valuable when constrained/informed with the right data, systems and tools. So when someone asks you about your organization's "AI harness," they aren't being weird (okay, well, geeky maybe - but not weird). They might just be onto something... Diginomica picks - my top stories on diginomica this week * Tokenomics - the worldview according to Palantir as CEO Alex Karp lays into OpenAI and Anthropic's "effing insane" business models - Now here's one I was waiting for in our tokenomics series, and it's everything you'd expect, in that outsized way. Stuart quotes Palantir CEO Alex Karp: "What technical customers want is control over their compute, their models, their data stack, and their alpha. They want to know they own the means of production, that it's not being transferred to someone else. They're not interested in some fake deploy that somehow is deploying tokens that transfers the alpha to a third party. The jig is up." Also see: Stuart's Tokenomics - the Qualcomm worldview as a $3.9 billion data center gambit starts to add up. * AI and Security - if enterprises rush in where developers fear to tread, what's the answer? - Chris gets into the crux of the AI security tensions, via new survey data from Aikido, and contrasting interviews: "Often, the tech industry's response is to say that only AI can solve the problem of AI and face down its disruptive tendencies and security holes: fight fire with fire. But earlier this year, my interview with ThreatLocker CEO Danny Jenkins at Zero Trust World in Orlando suggested it is not as simple as that." * Social intelligence vs AI slop? Here's what brands are getting wrong - Barb parses some fresh AI data from Sprout Social: edutainment for the win. "Avoiding AI slop isn't just about using less AI; it's about creating content that audiences actually want to engage with." Barb notes: "The quality of AI-generated content depends on the quality of the input content." Based on my recent research experiments, I'll agree, but with this caveat: it also depends on whether humans can correct/fix/adjust/edit the output. Some AI creation tools have very few editing/correction features. * Robots don't have fun! How an AI+human paradigm shift is essential to turbo-charged brand-building at Procter & Gamble - Stuart explores the fusion of AI and human creativity in the same brand processes. He quotes Chief Brand Office Mark Pritchard: "The brand's voice requires a human insight that's translated into a creative brand idea and a trusted point of view from the heart of that brand. The expert voice runs on human credibility, and the consumer's voice is the most genuine of all, because it's someone like me who I really trust. AI and algorithms can certainly amplify these voices at scale, but they really don't originate them." Vendor analysis, diginomica style. Here's my three top choices from our vendor coverage: * Why Appian CEO Matt Calkins thinks AI will make low-code less important - and its platform more valuable - Ian on Appian's platform re-invention: "Appian's ambition, then, is not to defend low-code from AI systems, but to make itself an indispensable infrastructure layer for the AI systems that threaten to displace it." * As isolved updates agentic AI, CEO Michael Haske explains the new developments - Brian has an isolved update for us, and AI agents for HR processes are front and center. * Config 2026 - Weave brings a new layer of precision design workflows to Figma - Phil was on the ground for Figma Config 2026. Here, he brings us the Weave angle: "Just as ERP serves as the system of record for enterprise transactions, Figma can be thought of as the system of record for enterprise design -- the platform where the precise look and feel of a brand or a product is set down. The addition of Weave brings crucial control over that precision at a time when generative AI introduces new scope for inadvertent deviation." A few more vendor picks, without the quotables: Jon's grab bag - Alyx has the lowdown on the Linux Foundation's latest project in OpenSharing extends Delta Sharing to AI assets - and stops where your contracts begin. Meanwhile, Stuart brings us all the news we missed in The long and the short of IT - the week in digibytes. Remote work has carbon impacts to reckon with. Cath examines the issues in The future of work - is 'slowmadism' the answer to cutting the carbon cost of remote work? Stuart's latest use case takes a broader view of UK innovation: "The best job at the bank" - NatWest CIO Scott Marcar on AI impact, CX centricity, and how to support UK innovation. Brian has some serious challenges for HR tech vendors in Challenge Brian! HR tech solutions needed - only relevant candidates need apply! Mark Chillingworth has a new diginomica network profile for us in CTO Nick Andrews delivers digital infrastructure for Norsk-Global. Finally, Chilingworth also has a fresh batch of diginomica network research for us in the diginomica network data - EU AI Act needs more CIO attention: Along with training demands, the EU AI Act requires firms to have a clear inventory of every AI tool and integration that is operating across the enterprise. Almost half (47%) of our community has achieved this, with some gaps, and a little over a quarter (27%) have partial visibility, and just under a quarter (23%) have fully mapped AI across the entire business. More on this one next week... Best of the enterprise web My top eight * The 'Tokenpocalypse' is here: Companies quietly throttle AI as token bills pile up - the answers to this will come; some of them are addressed in this week's edition (read on), but, for now - we're in the wild west of gen AI ROI. * Claude Code hijacked via Sentry -- Datadog, PagerDuty at risk - Looks like Louis Columbus doesn't get the summer off: "A single fake error report hijacked Claude Code in controlled testing -- the agent ran the attacker's code with the developer's full privileges, and not one alert fired. EDR, WAF, IAM, and the firewall all missed it completely." * AWS launches forward deployed engineering unit with $1 billion investment - Don't you love FDEs? Larry Dignan quotes Constellation's Ray Wang, who sounds like he's had enough of the bombast too: "I'm tired of looking at fake FDEs. A real FDE understands how to take the requirement and put it back into the product and actually get something done. These aren't glorified sales consultants or sales engineers." * Risk Register Governance: Spotting Quiet Closure Before It Costs You - Ted Rogers is rocking it over at UpperEdge, with some of the most trenchant project posts of the year - and I don't use 'trenchant' lightly. * The Illusion of the AI Copilot: Why Your Legacy CRM Architecture Isn't Cutting It - Thomas Wieberneit has a strong critique of legacy-style CRM. * If CRM Is Dead, How Is the Relationship Still Breathing? - and Constellation's Liz Miller has a different take, but they are both about rethinking. But the baby and the bathwater are two different things... * Why cheaper models alone won't save your AI budget - useful lessons here... Bottom line: agentic loops are a token hog, and system engineering is non-negotiable, unless you want to get stuck with the whole tab at the end of dinner: "Poorly designed agent loops or inefficient multi-agent handoffs can dominate costs in ways that are invisible when you're only looking at per-request pricing." * Systems Over Scale: What Bridgewater Teaches Us About the Enterprise AI Plateau - Speaking of better ways forward, Vijay Vijayasankar builds on that theme: "[Bridgewater] took an open weight model, Qwen3-235B, and ran it through a serious reinforcement learning and distillation pipeline built with Thinking Machines Lab. The result was 84.7% accuracy on their internal financial evaluation suite at a fraction of the inference cost of the big commercial models. Those are impressive numbers. But the numbers aren't really the story. The story is how they got there." * Bonus multi-media pick: Enterprise month in review - is HR tech falling short? With Meg Bear and Amy Wilson - if you want to catch Bear and Wilson, of the Meg and Amy show, doing their unscripted reactions to Brian's HR tech beefs above, check this replay. Whiffs Err, this is awkward: Come to think of it, so is this: I promise I don't seek Microsoft out for the whiffs column, but when in Rome: See you next time... If you find an #ensw piece that qualifies for hits and misses - in a good or bad way - let me know in the comments as Clive (almost) always does. Most Enterprise hits and misses articles are selected from my curated @jonerpnewsfeed.

[8]

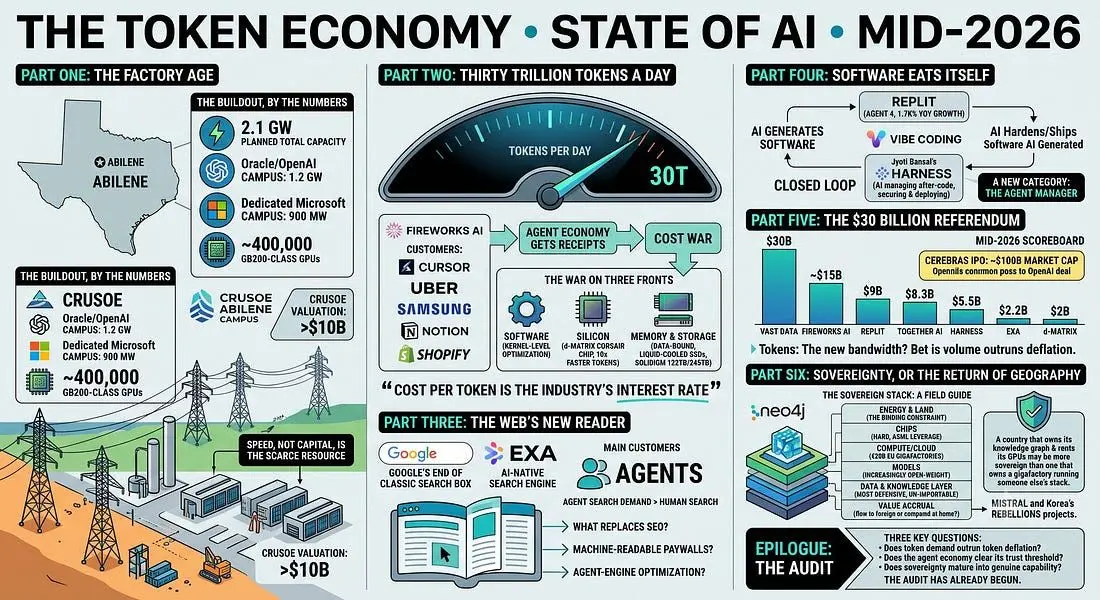

The token economy: The state of AI mid-2026

Gigawatt factories in the Texas scrub. Thirty trillion tokens a day. A $30 billion storage company, a search engine built for machines, and a continent trying to buy its independence one graphics processing unit at a time. Three years after ChatGPT, the artificial intelligence business has stopped being a demo and started being an economy -- and the economy is about to get audited. Drive west out of Abilene, Texas, and the future of the technology industry announces itself the way heavy industry always has: earthworks, transmission lines and steel going up faster than seems entirely plausible. On more than 980 acres, Crusoe Inc. -- a company that began its life burning waste natural gas to mine bitcoin -- is building what may be the largest concentration of computing power ever assembled. The first phase is live, serving Oracle Corp.'s and OpenAI Group PBC's Stargate program. The expansion underway takes the campus to 1.2 gigawatts. In March, Crusoe announced a second, adjacent 900-megawatt campus dedicated to Microsoft. Full buildout points toward 2.1 gigawatts on a single site -- roughly the output of two nuclear reactors, feeding on the order of 400,000 top-shelf GPUs. It is worth pausing on what that is. Not a data center in the old sense -- a beige building humming politely at the edge of a suburb -- but a factory, in the literal sense the industry has now adopted without irony. Energy goes in one end; intelligence, metered in tokens, comes out the other. Crusoe raised $1.375 billion in late 2025 at a valuation north of $10 billion, with more reportedly coming, and secured 4.5 gigawatts of natural gas through a joint venture to keep the production lines fed. The company's founding insight -- put compute where energy is cheap and stranded, because moving electrons is harder than moving data -- has gone from a crypto-era arbitrage to the organizing principle of a global buildout. This is a report on the state of that economy: where the money is going, what the machines are actually doing, and the three questions that will decide whether mid-2026 is remembered as the moment the industry matured -- or the moment it peaked. Energy goes in one end; intelligence, metered in tokens, comes out the other. Part 1: The factory age Crusoe's trajectory illustrates the whole category. Its founders -- a quant trader and an energy scion -- began by capturing flared gas at oil wells, an environmental fix that doubled as cheap power. When AI demand detonated, the same logic scaled: Don't bring energy to the compute, bring compute to the energy. The result is that the biggest names in software -- OpenAI, Oracle, Microsoft Corp. -- now anchor their most ambitious infrastructure on a company that was, five years ago, a clever footnote in the bitcoin story. Hyperscalers with hundreds of billions in capital spending budgets still cannot build fast enough, and speed, not capital, has become the scarce resource. The factory age has a price beyond capital, and it is measured in megawatts and methane. Crusoe's 4.5-gigawatt gas joint venture sits awkwardly beside its climate-aligned origin story, and the company is hardly alone: Across the industry, the power hunger of AI has quietly rewritten the sustainability commitments of nearly everyone involved. The honest framing -- one the industry is only beginning to say out loud -- is that the buildout is being financed on the assumption that intelligence is worth more than the externalities of producing it. That assumption may be right. It has not been demonstrated. And behind it lurks the bear case that every infrastructure veteran carries like a scar: the fiber glut of 2000, when a genuine technological revolution nonetheless incinerated the capital of the companies that built its plumbing. The skeptic's syllogism is simple. Demand projections are stacked on demand projections; some financing is circular, with chipmakers investing in the clouds that buy their chips and model labs committing to capacity they will pay for with money raised against the value of those very commitments. If token demand merely grows very fast -- rather than absurdly fast -- a meaningful share of the gigawatts under construction will open into a glut. The counterargument is the rest of this report: Unlike fiber in 1999, the capacity being built in 2026 is sold out before it is energized, by customers with revenue. Which makes the real question not whether the factories will be used, but whether the businesses using them make money. For that, you have to follow the tokens. The buildout, by the numbers * 2.1 GW -- planned total capacity of Crusoe's Abilene site across the Oracle/OpenAI campus (1.2 gigawatts, phase two completing 2026) and the dedicated Microsoft campus (900 megawatts, first building energized mid-2027). * ~400,000 -- GB200-class GPUs the full Abilene build can host across eight buildings on 980+ acres. * 4.5 GW -- natural gas capacity Crusoe secured via joint venture with Engine No. 1. * $1.375B -- Crusoe's Series E (October 2025), at a valuation above $10 billion. * ~€20B -- the EU's AI gigafactories initiative via EuroHPC, targeting facilities of ~100,000 processors each. Part 2: 30T tokens a day: The agent economy gets receipts Thirty trillion tokens is not a chatbot statistic. Numbers like that happen when software calls software: coding agents that decompose a request into hundreds of model calls; support agents that read, reason, retrieve, and write in loops; pipelines where one user click detonates a cascade of inference. 2026 was widely nominated, at last year's conferences, as the year agents would go from demo to production. The token data says the nomination was accepted -- with an asterisk. Agents went to production where the economics worked, and the economics work only where the cost per task is low enough. That is why the defining competition of this phase of the industry is not a capability race but a cost war. The war is being fought on three fronts at once. The first is software: kernel-level optimization of the kind Fireworks and its rival Together AI Inc. (which closed an $800 million round at an $8.3 billion valuation on July 1, on annualized bookings above $1.15 billion) treat as core intellectual property. The second is silicon. Fast growing d-Matrix Inc., a Santa Clara chipmaker founded by networking silicon veterans Sid Sheth and Sudeep Bhoja, spent seven years betting that inference's villain is the memory wall -- the energy and time wasted shuttling data between processor and memory -- and moved the math into the memory itself. Its Corsair accelerator entered full production in June, shipping in volume, with rack-level claims of roughly 10 times faster token generation at a third of the cost and a fifth of the energy for latency-sensitive work, and an independently verified demonstration cut a 24-second response to under two. Notably, d-Matrix does not propose replacing the GPU but pairing with it -- a coexistence strategy that says something about how mature this market has become: The challengers are no longer storming the castle; they are leasing rooms in it. The third front is the humblest and, increasingly, the most surprising: memory and storage. Solidigm, the SK hynix Inc. subsidiary shipping 122-terabyte solid-state drives with 245-terabyte models on the 2026 roadmap, has spent the year evangelizing a heresy that is quietly becoming consensus: AI data centers are becoming data-bound, not compute-bound. Agents with million-token contexts generate enormous key-value caches that must live somewhere fast; retrieval pipelines hammer storage in patterns training never did. When the industry's hottest thermal-engineering project is a liquid-cooled SSD co-designed with Nvidia Corp., the definition of "AI infrastructure" has officially expanded beyond the GPU. Stitch the three fronts together and the strategic picture clarifies. Cost per token has become the industry's interest rate -- the single variable that decides which agent business models clear. Every percentage point it falls, some previously impossible product becomes viable, and some incumbent's pricing becomes untenable. The companies profiled here are not competing to make AI smarter. They are competing to make it cheap enough to be everywhere. History suggests that is the more lucrative ambition. Cost per token has become the industry's interest rate -- the variable that decides which business models clear. Part 3: The web's new reader Exa's thesis, articulated by co-founder Will Bryk, is that as agents proliferate, machine search demand will grow to hundreds or thousands of times human search volume -- software researching, comparing, verifying and citing at a scale no population of humans could match. The company's embeddings-first index already answers queries for Cursor, Cognition, HubSpot and more than 400,000 developers, at speeds (sub-180 milliseconds) tuned for programs that fire dozens of searches per task. Bryk has argued agents will outsearch humans within the year. His valuation -- tripled in under 12 months -- suggests investors believe him. The second-order consequences are the interesting part, and nobody in the industry has honest answers yet. The web's economic engine is a grand bargain: Content is free because humans see ads next to it. An agent does not see ads. If the primary readers of the open web become machines -- extracting facts, synthesizing answers, never clicking -- the bargain collapses, and with it the funding model for the content the machines are reading. Publishers already feel the leak; the lawsuits and licensing deals of the past two years were the opening skirmish. What replaces search-engine optimization -- agent-engine optimization? machine-readable paywalls? per-crawl micropayments? -- will decide who gets paid for knowledge on a web where attention is no longer the currency. There is a sovereignty subplot here too, easy to miss and hard to unsee: If a handful of American indexes become the memory through which every agent on earth understands the world, that is a concentration of epistemic power that makes the old debates about social-media algorithms look quaint. Europe noticed. It tends to notice these things about a decade before it does anything, but it noticed. Part 4: Software eats itself The most visible cultural fact of the 2026 software industry is that the people writing software increasingly aren't software people. Replit Inc. -- the browser-based coding platform that became the flagship of what the industry affectionately calls vibe coding -- raised $400 million in March at a $9 billion valuation, triple its price six months earlier, on annualized revenue estimated about $525 million and a public ambition to reach a billion-dollar run rate by year-end. Users from 85% of the Fortune 500 build on it, most of them far from the information technology department. Its Agent 4 runs multiple coding agents in parallel on a single project; its president and head of AI, Michele Catasta, has framed 2026 as the year of the "agent manager" -- the worker whose job is not to make things but to direct, review and orchestrate the fleets of software that do. It is a genuinely new labor category, and it is arriving faster than the institutions around it. Which is precisely the alarm being rung, from the other end of the software lifecycle, by one of enterprise software's most credentialed founders. Jyoti Bansal built AppDynamics Inc. and sold it to Cisco Systems Inc. for $3.7 billion; his current company, Harness -- freshly funded with $240 million led by Goldman Sachs Alternatives at a $5.5 billion valuation, past $250 million in annual recurring revenue -- is built on an inversion of the vibe-coding story. AI made writing code nearly free, Bansal's thesis goes, but writing code was never the expensive part. Testing, securing, deploying and governing it -- everything after code -- consumes some 70% of engineering effort, and the AI code flood is making that bottleneck catastrophically worse. Harness' answer is to aim AI agents at the after-code lifecycle itself, reasoning over a knowledge graph of the entire delivery system: services, deployments, tests, incidents, policies, costs. Read together, Replit and Harness describe a single closed loop that may be the most important industrial dynamic of the decade: AI generates the software, and AI must then inspect, harden and ship the software AI generated. Optimists hear compounding productivity. Pessimists hear a system removing its own circuit breakers. Both are describing the same machine. What is no longer in dispute is the direction: the marginal cost of creating software is collapsing toward the marginal cost of describing it, and every assumption built on software being scarce -- org charts, vendor pricing, the profession of programming itself -- is now up for renegotiation. AI generates the software -- and AI must then inspect, harden, and ship the software AI generated. Part 5: The $30B referendum Vast is not an outlier; it is the pattern. Fireworks reportedly heading toward $15 billion. Replit at $9 billion. Harness at $5.5 billion. Exa at $2.2 billion. D-Matrix at $2 billion. Even the grizzled incumbents are being repriced: DataDirect Networks Inc. -- the profitable, 25-year-old workhorse that feeds xAI's hundred-thousand-GPU Colossus -- took $300 million from Blackstone at $5 billion and spent 2026 openly courting another strategic investor. DDN's coming valuation is a referendum, as one industry publication put it, on how the market prices the unglamorous parts of AI. What makes mid-2026 different from every prior stretch of AI exuberance is that the market now has a public comparison. Cerebras Inc., the wafer-scale chipmaker, went public in May, raised $5.55 billion in the year's biggest IPO, and watched its market capitalization approach $100 billion. The offering did two things at once: It validated the thesis that inference is a generational market, and it started the clock for everyone still private. Public markets are patient with stories exactly until a comparable company starts reporting quarterly numbers. The private cohort's revenue growth -- Fireworks nearly tripling in five months, Replit's 1,700% year-over-year, Together's 10-figure bookings -- is real and extraordinary. So is the gap between those numbers and the valuations built on them. Growing into a 60-times multiple requires nothing to go wrong, in an industry where the price of the underlying commodity -- the token -- is engineered to collapse. That is the paradox the whole edifice rests on: Every company in this report is working furiously to make intelligence cheaper, while being valued as if the revenue from selling it will only compound. Both can be true -- if volume outruns deflation, as it did for bandwidth, as it did for compute. The bet of 2026 is that tokens are the new bandwidth. The audit arrives when the first of these companies files an S-1. The private repricing: Mid-2026 scoreboard * Vast Data -- $30B (Series F, April), $500M+ committed ARR, $4B+ cumulative bookings; Nvidia invested. * Fireworks AI -- ~$15B (reported round in progress), ~$800M annualized revenue (est.), ~30T tokens/day. * Replit -- $9B (Series D, March), ~$525M annualized revenue (est.), targeting $1B run-rate by year-end. * Together AI -- $8.3B (Series C, July 1), bookings above $1.15B annualized; Aramco Ventures led. * Harness -- $5.5B (December-announced round led by Goldman Sachs Alternatives), $250M+ ARR at 50%+ growth. * Exa -- $2.2B (Series C, May), 400,000+ developers; a16z led. * d-Matrix -- $2B (Series C), Corsair in full production June 2026; M12 and Temasek on the cap table. Public comp: Cerebras -- $5.55B raised in May's IPO, market cap approaching $100B, anchored by a reported $20B OpenAI compute deal. Part 6: Sovereignty, or the return of geography The checks are getting large. The EU's AI gigafactories initiative, backed by roughly €20 billion through the EuroHPC joint undertaking, aims at facilities with around 100,000 advanced processors each -- a fourfold leap over the current generation. Mistral, Europe's model champion, raised €1.7 billion in a round led by ASML -- the Dutch lithography monopoly investing in the French model lab, about as legible as industrial policy gets. And the Mistral Compute venture is bringing some 18,000 Nvidia GB300s online south of Paris as a sovereign cloud for European workloads, independent of American and Chinese hyperscalers. The pattern repeats globally: Korea's National Growth Fund made its first-ever direct investment in the chip startup Rebellions under a program officials call, without embarrassment, the "K-Nvidia project"; Gulf sovereign capital led Together AI's July round; Temasek sits on d-Matrix's cap table. Nation-states have become the anchor customers -- and anchor investors -- of the AI infrastructure market. And yet for all the money, sovereignty remains a slogan in search of a definition -- which is why the most useful contribution to the debate this year may be a piece of intellectual hygiene rather than hardware. A framework advanced by technologists at Neo4j Inc., the graph-database company whose knowledge-graph technology increasingly serves as the context layer for enterprise AI agents, cuts the fog with two questions. First: sovereignty of what, and to what end? Three concerns dominate -- the ability to carry out AI activities unimpeded by any third party; the security and independence of data at rest and in transit; and where the economic value accrues. Second: sovereignty for whom? Nation-states, enterprises and individuals have genuinely different needs -- a bank in Frankfurt worried about vendor lock-in is not the French state worried about strategic autonomy, and neither is a citizen worried about her data -- and conflating them produces policy that serves none. From those questions fall the practical corollaries: interoperability, open standards, open source and a clear-eyed view of which layers of the stack -- chips, cloud, models, data, the knowledge layer that gives agents their context -- must actually be sovereign, and which can be safely rented. The framework's quiet radicalism is the suggestion that the layer everyone ignores may matter most. GPUs are fungible; models are increasingly open; but the knowledge layer -- the curated, structured, proprietary context that makes an agent trustworthy, auditable and specific to its owner -- is the part of the stack that cannot be imported. A country, or a company, that owns its knowledge graph and rents its GPUs may be more sovereign than one that owns a gigafactory running someone else's stack. If Europe's €20 billion buys only hardware, it will have purchased the least defensible layer of the pyramid. The open-source question shadows all of it. Open-weight models are the natural sovereign stack -- inspectable, hostable, unencumbered -- and the commercial data now backs the intuition: platforms serving open models report usage tripling year over year, with open-source inference crossing the billion-dollar threshold. But the finest open weights still descend overwhelmingly from American and Chinese labs, which means "sovereignty via open source" is, for now, independence built on another civilization's foundations. It is better than dependence on their application programming interfaces. It is not yet autonomy. That gap -- between what sovereignty rhetoric promises and what the supply chain permits -- is the honest state of the sovereign AI project in 2026. A country that owns its knowledge graph and rents its GPUs may be more sovereign than one that owns a gigafactory running someone else's stack. The sovereign stack: A field guide A working decomposition of what 'sovereign AI' has to cover, and how hard each layer is to localize: * Energy and land -- the binding constraint. Europe's expensive power and slow permitting are a bigger obstacle than any technology gap. * Chips -- hardest to localize; even "European" silicon designs are fabricated at TSMC. ASML's investment in Mistral shows where Europe's real chip leverage lives: the tools. * Compute/cloud -- the current spending focus: EU gigafactories (~€20B), Mistral Compute's ~18,000 GB300s near Paris. * Models -- increasingly open-weight, but frontier weights still originate largely from U.S. and Chinese labs. * Data & knowledge layer -- the most overlooked and arguably most defensible layer: the context, graphs and institutional knowledge that make agents trustworthy -- and that cannot be imported. * Value accrual -- the endgame question: whether the economics of AI activity compound at home or flow to foreign platforms. Epilogue: The audit Three questions will grade the era. Does token demand outrun token deflation, so the factories fill and the multiples resolve? Does the agent economy clear its trust threshold -- the after-code problem, the auditability problem -- before its first spectacular public failure? And does sovereignty mature from procurement program into genuine capability, or calcify into expensive symbolism? The optimistic case notes that every prior computing buildout that looked like madness -- mainframes, PCs, fiber, cloud -- was eventually absorbed by demand nobody had modeled. The cautionary case notes that "eventually" bankrupted a lot of pioneers on the way. What distinguishes this moment from the manias it is compared to is the receipts. The revenue is real, growing at rates enterprise software has never seen. The workloads are real; the tokens are countable. The bet is no longer on whether the technology works. It is on how fast an economy can be rebuilt around the assumption that intelligence is cheap -- and on who is left owning the pipes, the factories and the knowledge when the price of thinking falls to the price of electricity. That audit has already begun. The S-1s will be the exam.

[9]

The (not so) Hidden Cost of Using GenAI: By Steve Morgan

It's no secret that during the first wave of GenAI adoption, most of the fees were hidden behind subsidised pricing, big allowances and a relentless focus on driving usage. The message to financial services and all other industries was clear: use more GenAI. No doubt excitement and experimentation with GenAI were the first levers for consumption, but we then shifted to a measurement and celebration of usage i.e. quantity over (potentially) quality, and the concept of "tokenmaxxing" was born. Claude itself, when you ask it, thinks the concept of tokenmaxxing is 'pretty absurd when you think about it.. It's like paying by the word and deciding to write 'the the the the' instead of just 'the''. But regardless of how questionable this approach can be, what I believe is worse, and taking full advantage of this is the hidden and unpredictable token tax that comes with using GenAI and agentic AI in everyday operations. When you couple this with sometime using GenAI when it is not the best tool for the situation you've a potential recipe for failure. Many companies - mine included - are encouraging staff to use the various GenAI tools in their day to day work. And I think the key thing missing is ensuring people are using the right kind of AI or technology tool for the right use case and situation. The GenAI tools are great at summarising, for example, but do you need to summarise a 2 page article or should you just read it? Where does the AI start and end and where does the OI (Organic Intelligence) begin or need to be used? Is it right that at JPMorgan, where employees are being encouraged to integrate AI into their daily work, the bank is reporting employees are spending more on tokens than their salary? There have been plenty of stories of companies like Uber, Walmart and the Royal Bank of Canada where their use of tokens has jumped beyond budgets and forecasts. RBC tokens jumping 500% from 2025 to 2026. The financial burden of tokens To put this into perspective, when you consult an LLM, the AI agent will interpret the request, decide which tools to use, retrieve data, evaluate results, retry failed steps, confirm conclusions, and then produce a response. Each of these steps uses tokens (also known as reasoning tokens) and the more complicated the task, the more tokens will be needed. So, despite the fact that per-token pricing has dropped, enterprise AI bills are on the rise mainly driven by the increase of complex tasks. Not only that but the amount of tokens you consume doesn't necessarily guarantee better outcomes. Banks may be under the impression that they are gaining a competitive advantage and lower pricing, but the reality is that their overall costs are building up without them realising. This also means that running agents at scale has become more expensive. Part of this can be the re-decisioning where it is not needed, just plain wasting effort. AI vs. OI (Organic Intelligence)? Who wins? There's no question that GenAI can beat - in terms of speed - OI. But interpretation, judgement, decision making and errors? Whilst human intelligence is fallible, the leading LLMs are still generating errors (sidebar... why the persistent use of 'hallucinations'? They aren't seeing things, just making mistakes plain and simple). But this is the wrong way of looking at it. I do think we should view the current LLMs and GenAI usage cases as being to augment and improve processes that involve people. Do you need your senior legal counsel to re-read all the briefing docs and memorandum to respond to a client query, or is it better to have a legal agent do that, summarise it and they review it? Trust and verify. Clearly, the latter is more efficient. But not every single step needs an AI agent either, as this could introduce cost and unpredictability to your business. In the banking world, this is also unwise due to the highly regulated nature of the processes. Most important processes in banking have policies, procedures, clear sign off and escalation paths. That doesn't mean you can't find use cases for GenAI and agentic processes, it just means looking in the right places where it will be the right use of the right technology and have the most benefit. Take for example card lending which is already one of the most automated processes (up to 90-95%) with no human touch delivering a digital and physical card. While agentic AI could enhance the remaining 5-10%, the efficiency gains are likely to be minimal. Besides, regulatory requirements and bank risk appetite will always require human oversight for certain decisions. You could add a coach to sit alongside your card assessor or card servicing staff, but probably bigger benefits to be had in areas with far less automation like say mortgages or commercial lending. Establishing sustainable AI - design time vs. run time The distinction between design time and runtime is important. Design time is where reasoning AI delivers the greatest value. It encourages creativity, problem-solving, and the development of processes that provide long-term benefits. Whereas runtime is focused on reliable execution and prioritises consistency, governance, and cost efficiency. Using reasoning AI to design workflows while depending on lighter-weight AI to execute them allows financial services to reduce token costs without compromising performance. In many cases, it can also improve reliability by ensuring processes are executed in a more consistent and controlled way. Sustainable AI is not about removing reasoning, but about being intentional about where it delivers value. There's also an energy use angle here in terms of compute but lets leave that for another time... The road ahead The next phase of AI adoption will not be driven by technical capabilities but by economic discipline and outcomes. Financial services should focus on delivering predictable outcomes, managing operational costs and reducing the token overhead associated with agentic AI solutions. And remember, success will not come from deploying the most AI, but from applying the right AI to the right business problem. Not every challenge requires an agentic approach! Instead, banks should choose the approach that best fits the use case, their current level of tech maturity and the outcomes they want to achieve. Those who design AI solutions with efficiency and outcomes in mind will be better positioned to control costs while building systems that are easier to govern, scale and trust.

[10]

Token Unmaxxing: AI's Price War Is Starting to Reshape the Trade