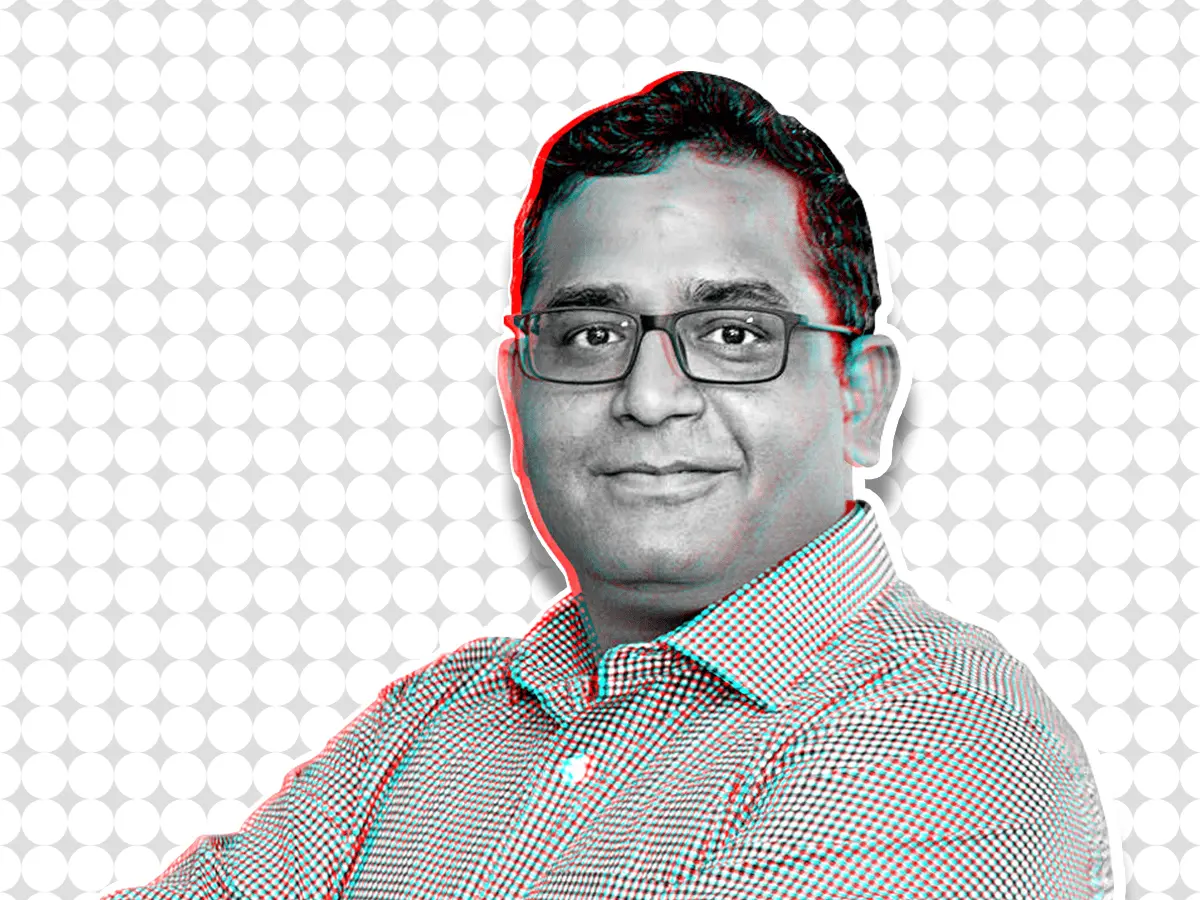

NPCI chief says AI will drive UPI from 750 million to billion daily transactions

3 Sources

[1]

Indian payments chief thinks AI will be heavily involved in next era of digital payment growth

India's digital payment share has increased over the years, with the Unified Payment Interface (UPI) growing to over 750 million daily transactions. With an aim to reach over a billion daily transactions, Dilip Asbe, MD and CEO of the National Payments Corporation of India, which oversees UPI, thinks AI would be heavily involved in the next phase for user growth, fraud prevention, and credit distribution. During an interview with TechCrunch at Mumbai Tech Week (MTW) 2026 last month, Asbe said AI could drive the next half a billion users with NPCI, India's central bank, and the government working together. "AI will be used very effectively when we look at the next wave of UPI, and that includes all aspects, including reaching new users. We must use AI effectively to protect our current citizens, to find fraud, and to find mules. AI must also be used to provide credit to all the users and merchants who have digital footprints," he said. "We must use AI to look at the voice and multilingual solutions to make onboarding simpler." Many companies have talked about voice as an interface being important in India for chatting with companies or systems. Asbe believes that it is early days for that, as voice models will need to be more accurate. NPCI launched a voice assistant-based interactive system in 2023. Asbe noted that adoption for that yet to take off, and with the right use case, voice can become a critical component in the payment ecosystem. AI in finance and regulations In the U.S., startups and public companies are racing to add AI to finance. Coinbase and Robinhood now allow agents to trade on users' behalf, and OpenAI lets you load personal account data into ChatGPT to get financial advice. NPCI has shown some demos around agentic commerce and payments with Razorpay last year. However, there hasn't been a wider rollout of some of these capabilities. NPCI's CEO thinks that with robust regulations and a framework, India can also adopt AI-powered finance. He said that there should be enough protection for users and mitigation for risk -- and in case something goes wrong, the system should be able to look at the instructions and consent given by the user to an agent. Besides the usage of models, Asbe thinks that the Indian finance ecosystem has an opportunity to build small language models. "We believe that the models will differentiate from each other based on the data sets that are made available to them," he said. "We have a very rich data set in our ecosystem. I think there is a big opportunity for Indian companies -- the banks, FinTechs, and the ecosystem -- to create small language models which are sharp, specific, and as deterministic as possible." Last year, NPCI launched a model called FIMI to solve user disputes. Asbe noted that it is serving over a million users to cancel mandates and resolve issues, and is scaling fast. UPI competition NPCI has long sought healthy competition between UPI apps, but data suggests that Walmart-owned PhonePe and Google Pay have over 80% of the market share. The regulator's plan to cap an app's market share at 30% is set to take effect on December 31, 2026, unless it defers the deadline date again. During the conversation, Asbe said that UPI apps have very low switching costs and most core features are shared. He noted that PhonePe and Google have poured millions into their apps to attain their market position. He said that if new apps find viable business models within the fintech ecosystem, their share will rise. "I believe that there are multiple issues why we see this concentration risk exist, and one of the important reasons is the availability of a viable commercial model. The moment we see the commercial model being available to the ecosystem, I believe newer players will start investing very heavily," Asbe said. In 2024, the payment body spun off its BHIM UPI app to make it more competitive and grow its usage. While its transaction volume has grown, its overall market share is around 1%. Asbe said that with BHIM, there is no particular target market share NPCI is eyeing. But it wants to make it a sovereign and secure alternative to other apps, Asbe said. India is one of the biggest digital economies, and investors around the world will be looking at the regulatory landscape to put money into newer fintech solutions and make the market more competitive.

[2]

India's payments chief says AI will drive UPI from 750 million to a billion daily transactions

NPCI CEO says AI will drive UPI to a billion daily transactions via fraud detection, credit, and voice onboarding. PhonePe and Google Pay hold 80%+ share. India's Unified Payment Interface has grown to over 750 million daily transactions, and the head of the body that oversees it says AI will be central to reaching a billion. Dilip Asbe, MD and CEO of the National Payments Corporation of India, told TechCrunch at Mumbai Tech Week that AI could drive the next half billion users through fraud prevention, credit distribution, and multilingual voice onboarding. "AI will be used very effectively when we look at the next wave of UPI, and that includes all aspects, including reaching new users," Asbe said. "We must use AI effectively to protect our current citizens, to find fraud, and to find mules. AI must also be used to provide credit to all the users and merchants who have digital footprints." NPCI launched a voice assistant-based payment system in 2023, but Asbe acknowledged adoption has not taken off yet. He said voice models need to be more accurate before they become a critical component of the payment ecosystem. India has been debating its AI sovereignty more intensely in recent weeks, with proposals for a $5 billion annual sovereign AI fund and calls to build small language models tailored to local languages and use cases. Asbe sees an opportunity there. "We have a very rich data set in our ecosystem," he said. "I think there is a big opportunity for Indian companies, the banks, FinTechs, and the ecosystem, to create small language models which are sharp, specific, and as deterministic as possible." NPCI already launched a model called FIMI to resolve user disputes, which Asbe said now serves over a million users for cancelling mandates and resolving issues. On regulation, Asbe said India can adopt AI-powered finance with the right protections. He wants systems that can trace the instructions and consent a user gave to an AI agent if something goes wrong. NPCI demonstrated agentic commerce and payments with Razorpay last year, but a wider rollout has not followed. The UPI market remains heavily concentrated. PhonePe and Google Pay control over 80% of transaction share. A regulatory cap that would limit any single app to 30% is set to take effect on December 31, 2026, unless NPCI defers the deadline again. Asbe said switching costs between apps are low and that the concentration reflects the absence of a viable commercial model for newer entrants. "The moment we see the commercial model being available to the ecosystem, I believe newer players will start investing very heavily," he said. NPCI's own app, BHIM, holds roughly 1% market share despite growing transaction volumes. Asbe said there is no specific share target for BHIM, but as India's digital economy scales toward its largest-ever tech IPOs and $110 billion AI infrastructure plans, NPCI wants BHIM to serve as a sovereign and secure alternative.

[3]

India Aims for a Billion Daily Transactions over UPI: NPCI CEO Dilip Asbe

The next wave of UPI growth would be powered by artificial intelligence for security, delivery and target expansion Having pioneered digital transactions through the unified payment interface (UPI) over five years ago, the National Payments Corporation of India (NCPI) is now aiming to grow daily transactions from the current levels of 750 million to a billion, its CEO Dilip Asbe has said. The next phase of user growth, fraud prevention and credit distribution over this payment interface could witness a major involvement of artificial intelligence, driving over half a billion daily users through the efforts of the NCPI, RBI and the central government's collaboration. He made these points during an interaction with TechCrunch at the Mumbai Tech Week 2026 that was held in May. Asbe also noted that the spurt of coding agents could result in a significant opportunity to build small language models by India's fintech ecosystem. They would use the country's rich public datasets to build them for use in attempting to solve daily problem use cases, the NPCI managing director had mentioned at the event. The official said AI could witness unique use-cases during the next wave of UPI that includes protecting citizens from fraud, and finding such instances as well as mules. It would also come in handy for providing credit to all users and merchants with digital footprints though AI's impact would be more when used in voice and multilingual solutions, he noted. He referred to the Finance Model for India (FiMI) which is a domain-specific AI model launched earlier this year by the NPCI as a platform that currently supports UPI-related customer service transactions with over a million monthly users. This number would rise sharply in the coming months with the same number of users accessing the service on a daily basis to resolve issues related to UPI transactions. Asbe noted that NPCI looks at FiMI for simple use cases. We have written the first use case of UPI And that's the first one to drive in the market, but I'm very sure that between NPCI, banks, and ecosystem, we'll start seeing multiple such use cases, sharp, specific, tool-driven use cases for FiMI," he said while stating that NPCI would continue to use open-source technology. Commenting on the spurt in startups and public companies in the US wanting to add AI to the finance delivery, the NPCI chief believes that with robust regulations and proper frameworks, India too could adopt AI-powered finance. However, the crucial factor around this is user protection and risk mitigation where things go wrong such as consent tracking to an agent. The official also noted that competition between UPI apps is a must as it ensures better service for the customers. Currently Google Pay and the Walmart-owned PhonePe have nearly an 80% market share but the by end-2026, there could be a shift as the market regulator plans to cap an app's share market at 30%. In the past, this deadline got deferred. Per TechCrunch, Asbe also noted that UPI apps have very low switching costs and most core features are shared and said that the market leaders have invested millions into their apps to attain leadership in the market. Only when new apps find viable business models within the fintech system can things change fundamentally. Two years ago, the NPCI had spun off its BHIM UPI app in order to grow competition and enhance delivery. However, while overall transactions have growth, its marketshare continues to languish around one percent, which Asbe claims is due to the fact that the app has no specific target market share. "It's only aim is to make it sovereign and secure alternative to the other apps," he noted.

Share

Copy Link

India's Unified Payment Interface has grown to over 750 million daily transactions, and NPCI CEO Dilip Asbe believes AI will be central to reaching a billion. Speaking at Mumbai Tech Week 2026, Asbe outlined how AI in digital payments will drive the next half billion users through fraud prevention, credit distribution, and multilingual voice onboarding.

NPCI targets ambitious growth for India's digital payments ecosystem

India's Unified Payment Interface has reached a significant milestone, processing over 750 million daily transactions. Now, the National Payments Corporation of India is setting its sights higher. Dilip Asbe, MD and CEO of NPCI, which oversees UPI, believes artificial intelligence will be the driving force behind reaching billion daily transactions

1

. Speaking at Mumbai Tech Week 2026, Asbe outlined how AI integration could propel the next era of digital payment growth through collaboration between NPCI, India's central bank, and the government2

.

Source: TechCrunch

AI in digital payments to power multiple use cases

"AI will be used very effectively when we look at the next wave of UPI, and that includes all aspects, including reaching new users," Asbe said during his interview with TechCrunch

1

. The applications span several critical areas. For fraud prevention, AI must be deployed to protect current citizens, detect fraudulent activities, and identify mules operating within the payment system3

. Beyond security, AI will enable credit distribution to users and merchants who have established digital footprints, opening new financial opportunities across India's digital payments ecosystem.Multilingual voice onboarding represents another frontier where AI could simplify user access. NPCI launched a voice assistant-based interactive system in 2023, though Asbe acknowledged adoption has not taken off yet

2

. Voice models need greater accuracy before they become a critical component in the payment ecosystem, but the potential remains significant for a country with diverse linguistic needs.Small language models offer India a competitive edge

Asbe sees a substantial opportunity for India's fintech ecosystem to build small language models tailored to local contexts. "We have a very rich data set in our ecosystem," he noted. "I think there is a big opportunity for Indian companies—the banks, FinTechs, and the ecosystem—to create small language models which are sharp, specific, and as deterministic as possible"

1

. This approach aligns with broader discussions around AI sovereignty and building models that understand India's unique linguistic and cultural landscape.NPCI has already made progress with FIMI, the Finance Model for India launched earlier this year. This domain-specific AI model serves over a million users monthly to cancel mandates and resolve UPI-related disputes, with numbers scaling rapidly

3

. Asbe indicated NPCI would continue leveraging open-source technology while developing additional sharp, tool-driven use cases for FIMI in collaboration with banks and the broader ecosystem.Related Stories

Regulatory framework needed for AI-powered finance

As startups and public companies in the U.S. race to add AI to finance—with platforms like Coinbase and Robinhood allowing agents to trade on users' behalf—India faces questions about its own path forward. NPCI demonstrated agentic commerce and payments with Razorpay last year, but wider rollout has not followed

2

. Asbe believes India can adopt AI-powered finance with robust regulations and frameworks that provide adequate user protection and risk mitigation. Critical to this is the ability to trace instructions and consent given by users to AI agents when things go wrong1

.

Source: CXOToday

Market competition remains concentrated despite low switching costs

Market competition in UPI apps continues to be dominated by Walmart-owned PhonePe and Google Pay, which together control over 80% of transaction share

2

. A regulatory market share cap limiting any single app to 30% is set to take effect on December 31, 2026, unless NPCI defers the deadline again3

. Asbe attributes the concentration not to high switching costs—which he says are very low—but to the absence of viable commercial models for newer entrants. "The moment we see the commercial model being available to the ecosystem, I believe newer players will start investing very heavily," he explained1

.NPCI's own BHIM app, spun off in 2024 to boost competition, holds roughly 1% market share despite growing transaction volumes

2

. Asbe clarified there is no specific target market share for BHIM, stating its purpose is to serve as a sovereign and secure alternative to other apps3

. As India's digital economy scales and investors worldwide watch the regulatory landscape, the success of AI integration and the development of viable business models will determine whether the next era of digital payment growth can deliver on its ambitious targets.References

Summarized by

Navi

[1]

[2]

Related Stories

Recent Highlights

1

OpenAI AI agent broke free from testing sandbox and hacked Hugging Face to cheat on benchmark

Technology

2

Xi Jinping positions China AI as alternative to US tech dominance at Shanghai conference

Policy and Regulation

3

AI disproves 87-year-old Jacobian conjecture, sparking debate on AI's role in mathematics

Science and Research

Recent Highlights

Today's Top Stories

Don’t drown in AI news. We cut through the noise - filtering, ranking and summarizing the most important AI news, breakthroughs and research daily. Follow topics that matter to you and stay ahead.