Memory shortage crisis deepens as SK Hynix warns 2027 will be worst year for supply crunch

6 Sources

[1]

Memory makers are slaves to the boom-bust rollercoaster, and the AI boom is the wildest ride of all

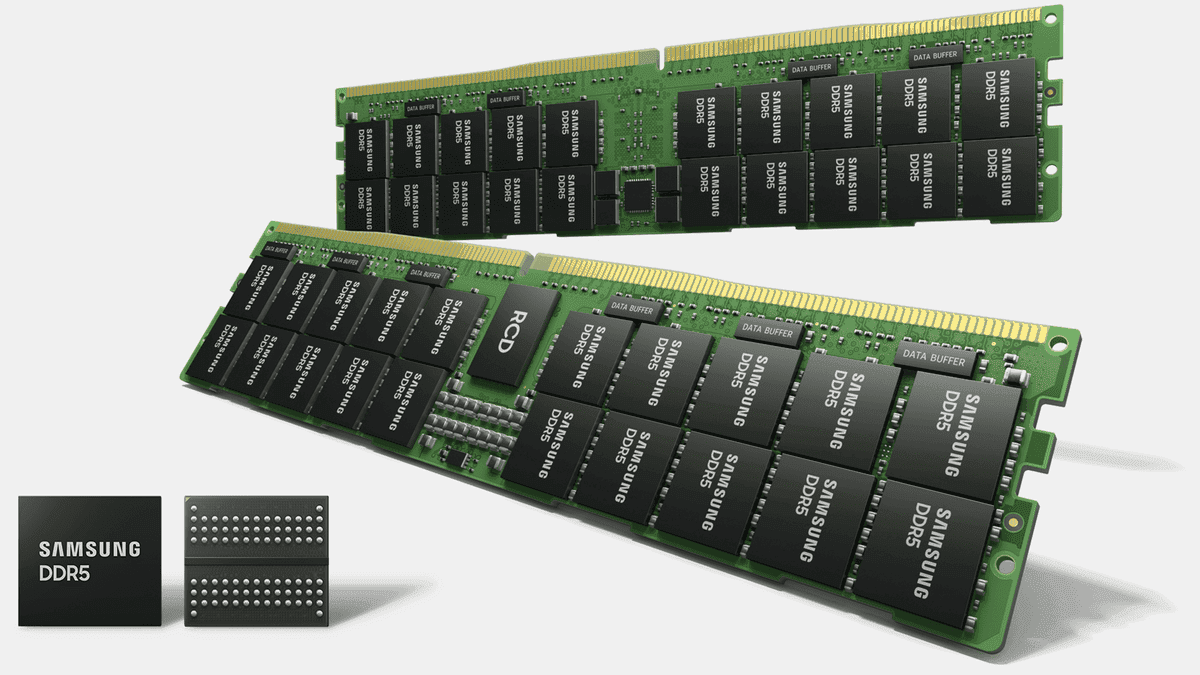

It's a good time to be in the memory business. As the AI datacenter business booms, SK Hynix and Micron's revenues have tripled in the last year, and Samsung's has roughly doubled. But while the trio have the AI revolution to thank for their good fortune, the deck is stacked for a reversal. Such is the memory business historically. Today, sky high demand for high-bandwidth memory (HBM), DDR5, and NAND flash memory needed for GPU servers has devoured any remaining capacity, leading to shortages that have driven up prices on everything from consumer electronics to AI infrastructure. You can't even buy a budget smartphone these days. The big three memory vendors are now in the process of investing hundreds of billions of dollars to bring new fab capacity online. In June, South Korean President Lee Jae Myung announced a $576 billion investment led by SK Hynix and Samsung to bolster chip production and shore up AI supply chains. On Thursday, Micron said that it would invest up to $3 billion to strengthen the US semiconductor supply chain, and according to recent reports, the Idaho-based chipmaker is also working to boost production across its Singapore, Taiwan, and Japan sites. Unfortunately, it's a slow process. Semiconductor manufacturing is among the most complex and resource-intensive industries in the world, and building a new DRAM or NAND flash wafer fab is not a trivial endeavor. Before the first chip can roll off the production line, financing must be secured, a location must been selected, permits must be won, and tens of millions of dollars of support facilities ranging from power conditioning and air handling to the ultra-pure water filtration systems must be deployed. Even after the clean rooms are completed, hundreds of millions of dollars of specialized lithography, wafer transport, and test equipment must be installed and validated. And once everything is ready to be powered on, it can take months to dial everything in and bring yields to acceptable levels. This process often takes years even without delays. So while there are a handful of new memory fabs already under way, anything SK, Samsung, or Micron starts today will take at least three years to bring online, and even longer to ramp production. That means memory prices are going to stay high for the foreseeable future. A recent IDC report warns that we may not see relief from the RAMpocalypse until at least 2028. That's great news for memory makers, whose revenues will stay inflated. But it's a big problem for AI startups and model devs, who will be paying higher infrastructure prices until that happens. OpenAI and others have spent the last four years or so and hundreds of billions of VC capital developing ever more capable models, agents, and tools. It's no longer a matter of whether the technology works, but rather whether the benefits justify continued investment at current or higher levels. Sooner or later, these startups will have to turn a profit, and sky high memory prices certainly aren't helping to find anything resembling a margin in the cost per token. The question now is whether or not the memory vendors can bring new capacity online before the great AI houses exhaust their VC-subsidized runway and the music stops. Historically, memory is a commodity, with wild swings in pricing characterized by boom and bust cycles. Memory vendors therefore rely on boom cycles to finance fabs, knowing full well that, once they come online, the additional capacity could end up cratering prices. As we reported late last year, the AI boom has changed this dynamic dramatically. Where we should have expected memory prices to fall across 2025 and 2026, we've seen the exact opposite as AI infrastructure consumes every bit of DRAM and NAND it can get its hands on. But if the anticipated demand for AI falls short, everyone loses and memory vendors will find themselves at the bottom of a bust cycle to end all bust cycles. On a bright note, the sky-high price of memory will no longer factor into why you can't afford a new laptop or smartphone. ®

[2]

The AI memory crunch won't ease until 2028

The AI build-out has snapped the memory market's decades-old boom-bust cycle, sending prices soaring when they should be falling. Relief is not expected before 2028, and if AI demand ever disappoints, the makers who are getting rich today could face a historic crash. The AI boom has broken the memory market's oldest rule. Prices that should be falling are soaring instead, and the AI memory crunch will not ease until 2028. The hangover, when it comes, could be brutal. Memory is meant to be boring. For decades DRAM and NAND flash have behaved like any commodity, sliding through predictable booms and busts as new factories flood the market and crater prices. That cycle has now snapped. As The Register lays out, the AI build-out has devoured every spare chip, and the result is an AI memory crunch with no quick way out. The cycle that broke By the old rules, 2025 and 2026 should have been a down-year. Prices should have drifted lower as supply caught up. Instead they climbed. GPU servers need vast amounts of high-bandwidth memory, DDR5 and NAND, and that demand has swallowed the lot. The knock-on has reached the shelf, pushing up the cost of consumer electronics and, as The Register puts it, killing the cheap smartphone. For the makers it is a windfall. SK Hynix and Micron have tripled their revenues in a year, and Samsung has roughly doubled its own. A fix measured in years The obvious answer is more factories, and the money is moving. In June, South Korean President Lee Jae Myung announced a $576bn drive led by SK Hynix and Samsung. Micron said last week it would spend up to $3bn shoring up its US supply chain, with more going to Singapore, Taiwan and Japan. None of it arrives soon. A new memory fab is one of the hardest things in industry to build, from permits and ultra-pure water systems to lithography tools that take months to tune. Anything started today needs at least three years to come online and longer to reach full capacity. The analyst firm IDC does not expect relief until 2028. Everyone downstream pays Until then, the cost lands on everyone below the memory giants. Chipmakers are already redesigning around the shortage. Samsung is readying a budget solid-state drive that strips out its onboard DRAM entirely, TechRadar reports, borrowing a slice of system memory to keep the price down. The AI companies feel it too. Every model developer renting AI infrastructure is paying more for it, which is poison for margins already stretched thin. The labs have spent four years and hundreds of billions in venture capital. They still have to turn the cost per token into a profit, and dearer memory makes that sum harder. The bust nobody is pricing in Here is the trap. Memory vendors finance their giant fabs on the strength of a boom. They know full well that when the new capacity finally switches on, it can flood the market and collapse prices. That is the cycle, and AI has only made the swing wider. The whole edifice rests on one assumption, that demand for AI keeps climbing. If it falls short just as the new fabs ramp, the makers face what The Register calls a bust to end all busts. So the real race is not memory against demand. It is whether the fabs come online before the AI bubble deflates and the music stops. For Europe, watching from the sidelines of a supply chain it barely controls, the squeeze is a reminder of how exposed it is. The region is racing to build its own AI datacentres. Yet a handful of firms in Korea, Taiwan and the United States ration and price the parts to fill them. The RAMpocalypse is a good time to be a memory maker. It is a nervous one for everybody else, and the reckoning has only been deferred, not cancelled.

[3]

SK Hynix warns 2027 will be 'worst year' for RAM prices -- right as a damning report reveals something that will add fuel to the price-fixing lawsuit

The big three memory makers told us RAMpocalypse was the unavoidable side effect of the AI revolution. But with one massive report from the Bank of America, that main alibi may have just gone up in flames. So context, the AI Tax on tech has been insane recently with prices going up by an astronomical 700%, and the big three memory makers (Samsung, SK Hynix and Micron) have made serious cash off as the oligopoly that controls around 90% of the global DRAM market. They claim that the reason prices are skyrocketing is because the demand for high-bandwidth memory (HBM) for AI data centers is so massive, that consumer RAM supplies are naturally drying up. In response, a massive class-action lawsuit in California is calling their bluff and accusing them of price fixing. For these memory makers, the defense should be a simple one: "we aren't fixing prices, and we're building new fabs as fast as we can!" You've heard a lot of this over the past few months about plans to open new plants to make more memory. BUT, a bombshell new report has potentially demolished that defense. How this alibi collapses According to a South Korean news outlet, a Bank of America report just dismantled the promises of doubled memory production capacity by 2030 -- with SK Hynix only likely to bring about one-sixth of its planned new memory capacity online by 2028. Here's why: * Timeline: Setting up the advanced infrastructure needed for these plants is going to take upwards of a decade. * Process upgrades: At the same time as it's building new plants, the manufacturing technology needs to be updated in older ones, which impacts output. In late June, South Korean President Lee Jae-myung made the claim that production capacity will be doubled by 2030, which sounds great on paper. However, Bank of America's estimates claim this figure misses out the closure of older plants, and that doubling claim is way too optimistic. For the plaintiffs in the lawsuit, this is going to be a juicy piece of circumstantial evidence. If it can be proven that SK Hynix is moving in slow-motion and severely under-delivering on its capacity promises, that narrative of "doing everything they can" to meet consumer demand is dismantled. Instead, it strongly supports the core allegation: they're happy to keep supply choked and prices inflated permanently. They're not reading the room Adding insult to injury, the CEO of SK Hynix recently warned that 2027 will be the "worst year" for the memory shortage, and predicted the crunch will last until 2030. But if one thing is clear, consumers are not buying this spin anymore. "That CEO was probably struggling so hard not to look too happy as he gave this "grim outlook"," one user posted on the PC Master Race Subreddit. Across Reddit, the reaction has shifted from passive frustration to absolute cynicism, with calls to "prosecute the memory cartel again" ringing out across r/technology. The overarching sentiment? I knew we weren't crazy. The playbook is painfully familiar. Samsung and SK Hynix previously pleaded guilty to a massive DRAM price-fixing operation in 2005. Now, facing a historic lawsuit over the exact same behavior, it feels like they're trying to hide behind the AI boom. But with this latest report saying their shiny new fabs won't save us anytime soon, the curtain has been pulled back. The AI memory shortage isn't a tragic tech accident; it's looking more and more like a highly profitable, coordinated choice. And we are all footing the bill. Follow Tom's Guide on Google News and add us as a preferred source to get our up-to-date news, analysis, and reviews in your feeds.

[4]

Samsung, SK hynix, Micron ramp up capacity as demand for AI infrastructure outpaces supply

Global memory chipmakers are expanding production capacity to meet AI demand. Samsung, SK Hynix, and Micron are investing billions in new facilities. These companies aim to secure supply for high-bandwidth and DRAM chips. Industry experts anticipate continued tight supplies for several years ahead. Capacity growth will determine memory makers' future market performance. Global memory chipmakers, Samsung Electronics, SK hynix and Micron Technology -- are accelerating capacity expansion to capitalise on the artificial intelligence (AI) boom, as demand for high-bandwidth memory chips used in AI servers continues to exceed supply, as per Korea Herald. Citing World Semiconductor Trade Statistics, the report noted that the global semiconductor market will likely grow 90 per cent this year to USD 1.51 trillion. Additionally, the memory market alone is forecast to surge 250 per cent to USD 803.9 billion. "Combined industry investment this year is expected to reach about 200 trillion won ($129 billion), led by the top three memory makers," it said. These tech giants are increasing investment in new fabrication plants, advanced packaging and chipmaking equipment to secure capacity before additional supply comes online, the report added. Samsung is expanding its memory manufacturing capacity through new projects in Pyeongtaek and Yongin in Gyeonggi Province, as well as its integrated semiconductor hub in Gwangju-South Jeolla. Meanwhile, SK hynix plans to deploy the USD 26.5 billion raised through its Nasdaq listing to increase wafer production capacity and strengthen its advanced chip packaging capabilities. Following SK hynix's Nasdaq debut on Friday, SK Group Chairman Chey Tae-won said, "We announced that we would double our production capacity within five years, but every customer says that will not be enough," Korea Herald noted. At the same time, Micron is also stepping up investments as the United States intensifies efforts to expand domestic semiconductor manufacturing. The company has announced plans to invest more than USD 250 billion in the US by 2035, including the construction of new memory fabrication plants in New York and Idaho, along with an expansion of its existing facility in Virginia. However, the report highlighted, "Despite concerns that the AI boom may be nearing a peak, industry executives and analysts expect supplies of high-bandwidth memory and conventional DRAM to remain tight for years." As per analysts, the outlook for memory makers will depend "less on short-term pricing than on how quickly they can add capacity," the report said. Park Seung-young, head of portfolio strategy at Hanwha Investment & Securities, on 3PROTV said, "Supply matters more than demand in commodity memory," adding, "The key question is how fast capacity can grow."

[5]

SK Hynix CEO Warns 2027 Will Be Memory's "Worst Year" Ever, With Shortages Set To Outlast The Decade

SK Hynix CEO has warned that memory shortages will be at their worst in 2027 as it celebrates its trading debut on Nasdaq in Times Square. Memory Supply Won't See Any Sign of Relief Beyond 2030 As SK Hynix Signals 2027 To Be The Worst Year In Terms of Shortages Well, memory shortages have gripped all aspects of the tech industry, and it seems to have become the norm these days. As the supply crunch continues, the CEO of SK Hynix, one of the three largest DRAM producers, has said that things are about to get much worse for the memory market. ○ 25 Years of Challenges and AI Leadership Through HBM Innovation * Just 25 years ago, the company faced its most difficult moments in history -- including the risk of bankruptcy -- yet fought through the crisis with everything it had. The resilience and determination forged in those days have been the driving force behind the SK hynix of today. * Beginning in 2012, the company joined SK Group and began shaping the future together. Even when the future of advanced memory was uncertain, SK hynix recognized the need for a new technology -- HBM -- and became the first in the world to make it a reality. * Through relentless innovation, HBM has come to stand at the very heart of the AI revolution. * Today, building on its technology leadership spanning HBM, DRAM, and NAND Flash, SK hynix provides the core memory technologies that power AI infrastructure around the world. Talking to Reuters at the commemoration of SK Hynix's Nasdaq Trading Debut of its ADR, CEO Kwak Noh-jung stated that the memory industry will see its "worst-ever" supply shortages in the coming year (2027). SK Hynix has also forecasted that, given the current market demand, they will fall way short of fulfilling the market demand, and that will continue beyond 2030. SK Hynix Chief Executive Kwak Noh-jung said the global memory industry is heading for its worst-ever supply shortage in 2027, forecasting that demand for memory will continue to exceed the company's ability to produce it well into the next decade despite aggressive capacity expansion. "We forecast that next year will be the worst year in the industry's history from the supply perspective," via Reuters The comments from SK Hynix are in line with what Samsung and Micron executives have already said. Samsung has warned of 2027 being the worst year in terms of shortages and that things will continue this way till 2028 and beyond. Meanwhile, Micron has said that the current shortages are only the "first innings" and that both DRAM/NAND supply will be tight, as they are only able to meet 40-50% of the total market demand in the coming years. Heightened demand from AI customers and multi-year agreements further put pressure on the market. The big three DRAM makers have already prioritized premium DRAM segments such as HBM and LPDDR5X, while commodity memory such as DDR5, DDR4, and entry-level LPDDR RAM has taken a back seat. While these have boosted the profits of SK Hynix, Micron, and Samsung, they have devastated the consumer segment, which is facing the worst kind of price hikes that are affecting all sorts of components and platforms, including PCs, Smartphones, Consoles, etc. Focus on premium memory has also paved the way for Chinese DRAM and NAND makers to go all-in on production to meet the demands of domestic customers. Names such as CXMT (DRAM) and YMTC (NAND) are doubling their production capacities. SK Hynix, like Samsung and Micron, is also preparing to embark on a multi-year and multi-billion dollar expansion plan with new fabs and facilities being laid out across South Korea. SK Hynix is also considering the construction of Fabs in the US, Japan, and Southeast Asia, though the final plans are yet to be cemented. Micron recently started construction of its new facility that will be put towards DRAM production. Follow Wccftech on Google to get more of our news coverage in your feeds.

[6]

Global Market: SK Hynix warns of historic memory chip shortage by 2027 as AI demand soars

SK Hynix anticipates a severe global memory chip shortage extending beyond 2030. Accelerating artificial intelligence infrastructure demand fuels this projected supply constraint. The company is exploring new fabrication facilities in regions like the United States. South Korea plans significant domestic memory chip production expansion over five years. Record profits highlight SK Hynix's strong leadership in the AI memory market. SK Hynix expects the global memory chip industry to face its most severe supply shortage in 2027, with demand continuing to outstrip production capacity well into the next decade, according to comments by Chief Executive Kwak Noh-jung reported by Reuters. Speaking following the company's Nasdaq debut, Kwak said customer demand for memory chips continues to grow faster than the industry's ability to expand manufacturing capacity. Despite aggressive investment in new facilities, the company expects supply constraints to persist beyond 2030 as demand for artificial intelligence (AI) infrastructure accelerates. US MarketsPowered By As on 11 Jul 2026, 01:30 AM IST S&P 500 Top Gainers Meta Platforms669.21(5.97%) Weyerhaeuser23.45(4.22%) SBA Communications190.03(4.14%) NVIDIA210.96(4.03%) Gainers" S&P 500 Top Losers Moderna68.27(-10.83%) Coterra Energy32.56(-8.62%) CrowdStrike Holdings187.18(-5.66%) Datadog257.54(-4.26%) Losers" The warning underscores the structural imbalance emerging in the semiconductor industry, where AI-related applications are driving unprecedented demand for advanced memory products, particularly high-bandwidth memory (HBM). AI boom fuels SK Hynix's growth SK Hynix has emerged as one of the biggest beneficiaries of the AI revolution, establishing itself as a leading supplier of HBM chips used in Nvidia's AI accelerators. The South Korean chipmaker has gained a strategic position in the AI supply chain, helping power the rapid expansion of generative AI and cloud computing infrastructure. US among potential locations for future chip manufacturing Reuters reported that Kwak said the United States remains under consideration for a future wafer fabrication facility, although the company has yet to make a final investment decision. According to him, SK Hynix will prioritize regions that offer adequate land, reliable electricity and water supplies, a skilled workforce and competitive manufacturing costs. Besides the U.S., Japan and Southeast Asia are also being evaluated as potential locations for future expansion. Currently, the company operates major manufacturing facilities in Icheon and Cheongju in South Korea and is constructing a large semiconductor complex in Yongin. South Korea expands semiconductor manufacturing SK Hynix and Samsung Electronics are participating in South Korea's ambitious plan to significantly expand domestic memory chip production over the next five years. The government-backed initiative involves investments of approximately 400 trillion won ($266 billion) each in new semiconductor production facilities in the country's southwest. While the plan is designed to strengthen South Korea's leadership in memory chips, some investors have expressed concerns that such large-scale capacity expansion could expose manufacturers to cyclical downturns. In the United States, SK Hynix is already investing around $4 billion to build an advanced chip packaging plant in Indiana. Reuters also reported that the company plans to invest another $10 billion in developing AI-focused businesses in the U.S. to support future growth. AI investment concerns remain under scrutiny Although semiconductor stocks have recently come under pressure amid concerns that AI infrastructure spending may be nearing a peak, industry executives remain optimistic about long-term demand. Reports suggesting Apple is diversifying parts of its semiconductor supply chain and Meta is seeking to commercialize excess AI computing capacity have raised questions about the sustainability of AI-related investment. However, Reuters noted that Nvidia CEO Jensen Huang recently said shortages of AI memory are likely to continue for several years because demand remains exceptionally strong. He also indicated that SK Hynix is expected to remain Nvidia's largest memory supplier. UBS similarly forecasts that the global DRAM market will remain undersupplied until at least the second quarter of 2028. Wall Street remains bullish on AI infrastructure spending Bank of America also maintains a positive outlook on AI investment, estimating that global hyperscaler capital expenditure will reach about $851 billion this year before climbing to roughly $1.15 trillion next year. According to Reuters, the bank believes strong cloud demand, improving returns on AI investments and rising demand for compute-intensive AI applications will continue to support infrastructure spending. It also said that the approximately $244 billion raised by major hyperscalers this year reflects balance-sheet optimization rather than funding constraints. The positive outlook received another boost after Micron announced plans to increase its U.S. investment commitment to more than $250 billion through 2035, up from its previous $200 billion target, citing surging AI-driven demand for memory chips. Record profits highlight AI leadership The AI boom has transformed SK Hynix's financial performance. The company reported a record operating profit of 47 trillion won ($31 billion) in 2025, more than double the previous year's earnings and a dramatic turnaround from its operating loss in 2023. Analysts expect the momentum to continue. Reuters reported that LSEG SmartEstimate projects operating profit of approximately 65.5 trillion won for the April-June quarter. Despite an 18% decline in the company's share price over the past two weeks amid broader concerns about AI-related valuations, SK Hynix shares have surged more than sevenfold over the past year, reflecting investor confidence in its leadership in the rapidly expanding AI memory market.

Share

Copy Link

The memory chip industry faces its most severe supply crisis yet, with SK Hynix CEO predicting 2027 as the worst year for memory shortage. Despite hundreds of billions in fab investments by Samsung, SK Hynix, and Micron, relief won't arrive until 2028 at earliest. Meanwhile, a price-fixing lawsuit and damning Bank of America report challenge industry claims about production constraints.

Memory Chip Industry Faces Historic Supply Crisis

The memory chip industry is heading toward an unprecedented supply crisis, with SK Hynix CEO Kwak Noh-jung warning that 2027 will be the "worst year in the industry's history from the supply perspective."

5

The warning came as the company celebrated its Nasdaq trading debut, signaling that demand for memory will continue to exceed production capacity well into the next decade despite aggressive expansion plans. This grim outlook aligns with predictions from Samsung and Micron executives, who have similarly forecast that the memory shortage will persist beyond 2028.1

Source: Wccftech

AI Demand Breaks Traditional Boom-Bust Cycle

The AI boom has fundamentally disrupted the memory market's decades-old boom-bust cycle. Where prices should have fallen across 2025 and 2026 following historical patterns, they have instead soared as AI infrastructure consumes every available chip.

1

Sky-high demand for high-bandwidth memory (HBM), DDR5, and NAND flash memory needed for GPU servers has devoured remaining capacity, creating shortages that have driven up prices across everything from consumer electronics to AI infrastructure.1

The financial windfall has been staggering: SK Hynix and Micron have tripled their revenues in the last year, while Samsung's revenue has roughly doubled.1

Massive Investments Won't Deliver Quick Relief

The big three memory makers are pouring hundreds of billions into new production capacity, but semiconductor manufacturing timelines mean relief remains years away. In June, South Korean President Lee Jae-myung announced a $576 billion investment led by SK Hynix and Samsung to bolster chip production and shore up AI supply chains.

1

Micron committed up to $3 billion to strengthen the US semiconductor supply chain, with additional investments across Singapore, Taiwan, and Japan facilities.1

However, building new fabrication plants requires securing financing, selecting locations, winning permits, and deploying tens of millions of dollars in support facilities before installing hundreds of millions in specialized lithography equipment. Anything started today will take at least three years to bring online, with months more needed to dial in yields.1

An IDC report warns that relief from the memory shortage may not arrive until at least 2028.1

Source: ET

Price-Fixing Lawsuit Challenges Industry Narrative

A damning Bank of America report has potentially demolished the memory makers' defense against a massive class-action price-fixing lawsuit in California. The report reveals that SK Hynix will likely bring only one-sixth of its planned new memory capacity online by 2028, far short of promises to double production capacity by 2030.

3

Setting up advanced infrastructure for these plants will take upwards of a decade, while simultaneous process upgrades at older facilities will impact output.3

The lawsuit accuses the oligopoly controlling around 90% of the global DRAM market of keeping supply choked and RAM prices inflated permanently.3

Consumer frustration has intensified, with prices rising by an astronomical 700% and calls to "prosecute the memory cartel again" spreading across social media.3

Samsung and SK Hynix previously pleaded guilty to a massive DRAM price-fixing operation in 2005.3

Source: Tom's Guide

Related Stories

AI Startups Face Margin Pressure

Sustained high memory prices create serious challenges for AI companies already struggling with profitability. Model developers renting AI infrastructure are paying inflated costs, which damages margins on already-stretched cost per token calculations.

1

OpenAI and others have spent four years and hundreds of billions in venture capital developing models, agents, and tools. The technology works, but whether benefits justify continued investment at current or higher levels remains uncertain.1

These startups must eventually turn a profit, and sky-high memory prices make finding margin increasingly difficult. The critical question is whether memory vendors can bring new capacity online before AI companies exhaust their VC-subsidized runway and the music stops.1

Market Dynamics Point to Potential Bust

The entire memory market edifice rests on one assumption: that AI demand keeps climbing. If demand falls short just as new fabs ramp production, memory makers face what analysts call "a bust to end all busts."

2

Memory vendors historically finance giant fabs during boom cycles, knowing full well that additional capacity can flood the market and collapse prices once online.1

The AI boom has only widened this swing. According to World Semiconductor Trade Statistics, the global semiconductor market will likely grow 90% this year to $1.51 trillion, with the memory market alone forecast to surge 250% to $803.9 billion.4

Combined industry investment this year is expected to reach about $129 billion, led by the top three memory makers.4

Park Seung-young, head of portfolio strategy at Hanwha Investment & Securities, notes that "supply matters more than demand in commodity memory," adding that "the key question is how fast capacity can grow."4

For Europe, watching from the sidelines of a supply chain it barely controls, the squeeze serves as a stark reminder of its exposure as it races to build AI datacenters.2

References

Summarized by

Navi

[1]

[2]

Related Stories

RAM and Storage Prices Surge 500% as AI Demand Triggers Global Memory Crisis

26 Nov 2025•Business and Economy

Memory prices spike up to 400% as AI demand creates global shortage lasting through 2026

14 Dec 2025•Business and Economy

Memory shortage forces PC makers to raise prices up to 30% as AI demand drains supply

17 Mar 2026•Business and Economy

Recent Highlights

Recent Highlights

Today's Top Stories

Don’t drown in AI news. We cut through the noise - filtering, ranking and summarizing the most important AI news, breakthroughs and research daily. Follow topics that matter to you and stay ahead.